Top five consumer financial complaints reported across the U.S.

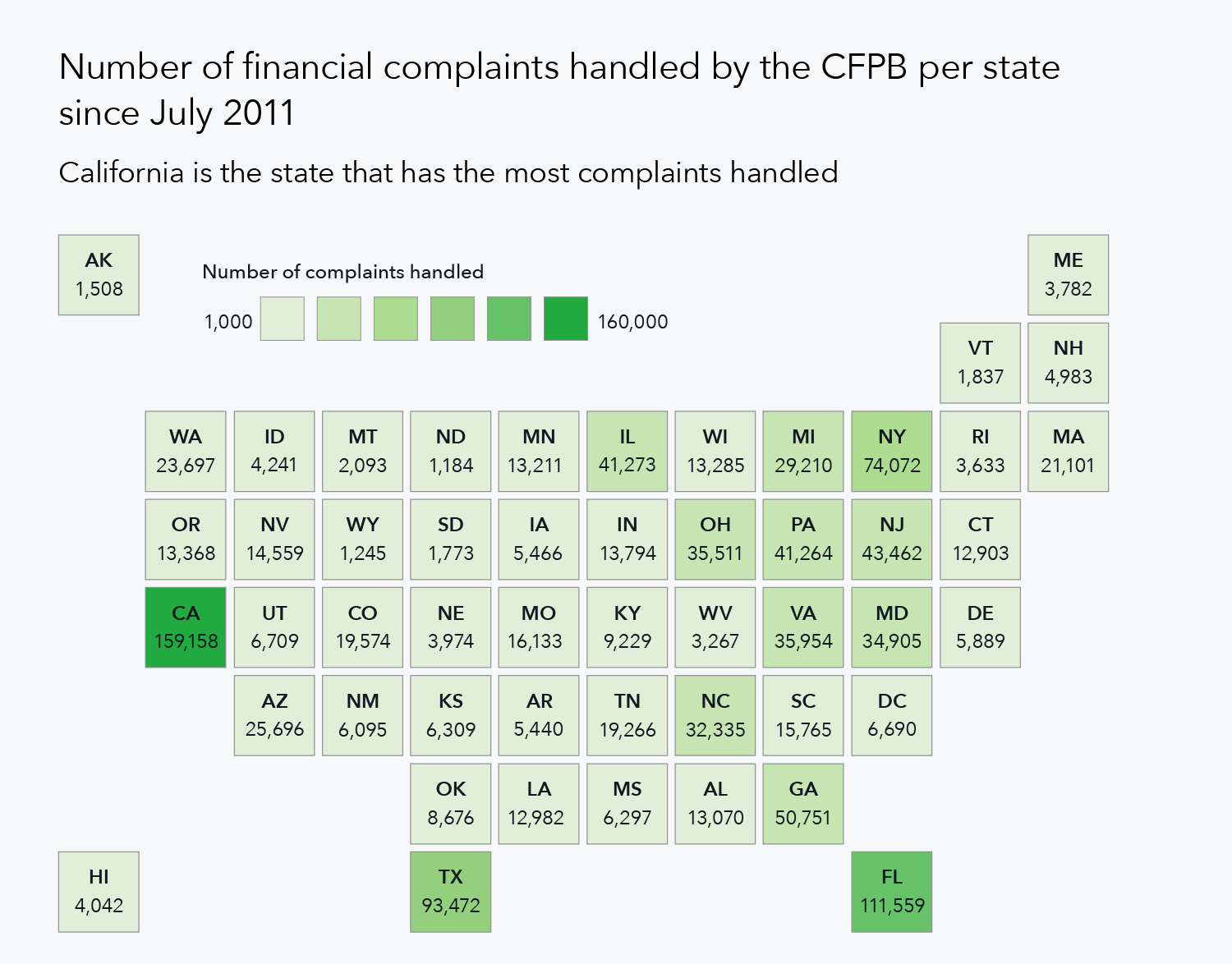

We recently released a special edition of our monthly complaint report that shares what we’ve been hearing from consumers from all 50 states and the District of Columbia.

While everyone’s personal financial situation is different, many consumers experience similar financial issues. Of the more than 1 million complaints we’ve handled since 2011, the top five types of complaints reported by consumers from all 50 U.S. states and D.C. are: debt collection, mortgages, credit reporting, credit cards, and bank accounts or services. We’re also sharing information you can use if you have issues that are similar to many other consumers.

1. Debt collection: Facing a debt you don’t owe

Twenty-seven percent of complaints we received were about debt collection. Many of those are specifically about repeated attempts to collect a debt the consumer did not owe. Here are steps you can take if you’re contacted about a debt that you don’t owe, that’s not yours, or that you need more information about. We also have sample letters you can use to respond to debt collectors.

2. Mortgages: Problems when you’re unable to pay

Among people submitting complaints about their mortgage, a common issue was problems they encountered when they were unable to make their monthly payments. If you can’t pay your mortgage, call your loan servicer right away. Your servicer may be willing to help you if you have missed a payment or are about to miss a payment. Use our checklist for more information on how to avoid foreclosure.

3. Credit reporting: Incorrect information on your credit report

Seventeen percent of complaints we received dealt with credit reporting, with the top issue being incorrect information on credit reports. Once you request your credit reports, it’s important to know what kind of information you should be looking for as you review them. Some common errors are incorrect account status, identity errors, and balance errors.

If you find an error, you should dispute it so that the error can be investigated. To dispute an error on your credit report, contact both the credit reporting company and the company that provided the information.

4. Credit card: Billing disputes with your credit card company

Of complaints about credit cards, more than 19,000 complaints were about consumers’ billing disputes with their credit card companies. If you need to dispute a charge on your bill, let your card issuer know about the problem right away.

You can call the card issuer, but to protect your rights you must also send a written billing error notice to the card issuer within 60 calendar days after the charge appeared on your statement.

5. Bank account or service: Account management questions

Ten percent of complaints submitted to the Bureau were about bank accounts or services. Our question-and-answer database covers solutions for common issues, such as avoiding overdraft fees.

More data from across the U.S.

Every month the Consumer Financial Protection Bureau handles more than 20,000 complaints. For a breakdown of top issues in a particular state or in D.C., check out the full report. We also have an overview of complaints from servicemembers and older adults.