Trends in Reported Assistance on Consumers’ Credit Records

This post is the second in a series documenting trends in consumer credit outcomes during the COVID-19 pandemic. Last August, we published a report on early trends in consumer credit outcomes through June 2020, which found largely positive trends in those outcomes despite widespread economic hardship due to the pandemic.

This post focuses on reported assistance on consumers’ credit records. For purposes of this analysis, we define consumer assistance as an account being reported with zero scheduled payment due despite a positive balance. In the August 2020 report, we found that most credit products saw a sharp uptick in assistance in March 2020 and an uptick in transitions out of assistance between April and June. Since July 2020, consumers have transitioned out of assistance to varying degrees across all credit products, but a significant share of mortgage borrowers continue to receive assistance.

As in the first post of this series, we use the Bureau’s Consumer Credit Panel (CCP), a deidentified sample of records from one of the three nationwide consumer reporting agencies. We focus on month-to-month transitions in assistance: loans that were reported with scheduled payment due in one month and no scheduled payment due in the next month despite a positive balance.

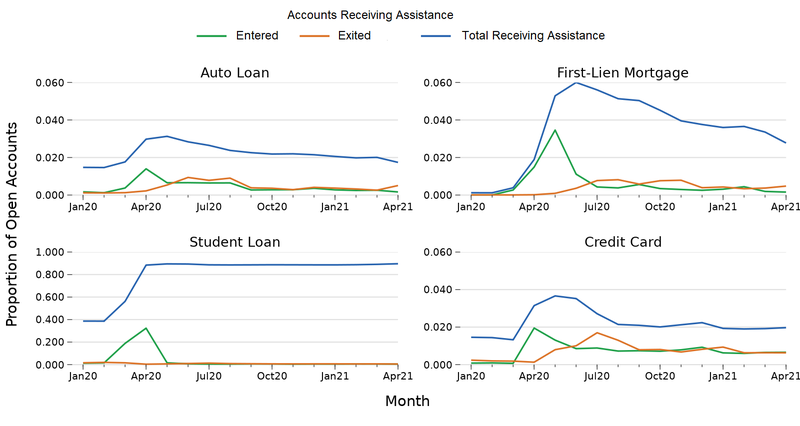

Most consumers have exited the payment assistance they received early in the pandemic

In the figure above, we report the total share of accounts with zero payment due (assistance) reported and month-to-month transitions into and out of assistance from January 2020 to April 2021. With the exception of student loans, the total share of loans with payment assistance began declining in the summer of 2020, as the initial increase in loans transitioning into assistance abated and accounts began transitioning out of assistance in larger numbers. There continued to be high rates of assistance in student loans largely due to the CARES Act, which put most student loans in automatic payment suspension. By March of 2021, the total share of auto loans and credit card accounts with assistance was only slightly above pre-pandemic levels, while the share of mortgages and student loans on assistance remains significantly higher than pre-pandemic baselines.

Consumers who exited assistance tend to live in communities hit harder by COVID-19

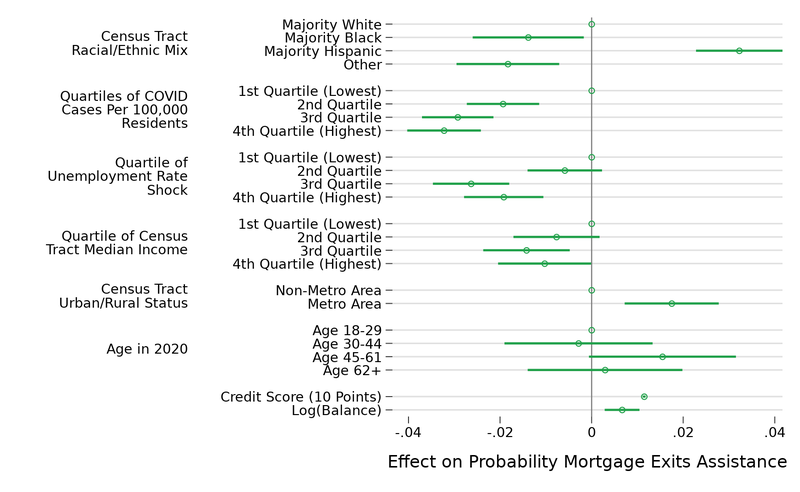

A substantial body of research has shown that some communities have been disproportionately affected by the health and economic shocks of COVID-19, and we anticipate those same disparities will be reflected in the likelihood that different groups receive and lose assistance. In the August report, we found that majority Black census tracts, majority Hispanic census tracts, older borrowers and borrowers in counties hit hardest by COVID cases and layoffs were most likely to receive assistance in the early months of the pandemic. This pattern has continued through March of 2021 (not shown). There is also substantial variation in which groups have exited mortgage assistance gained during the pandemic. In the analysis below, we focus on mortgage assistance, though in the August report we showed that patterns of assistance are relatively consistent across loan types.

In the figure above, we report the estimates of the probability that different populations of mortgage borrowers transitioned out of assistance they had received during COVID-19, holding other characteristics constant. For the categorical variables, the plotted points represent the average difference in probability that an account in that category transitioned out of assistance as compared to a reference category (indicated by a point at zero), holding all the other factors constant (see the August report for more details on the methodology behind this figure).

Consumers in Majority Hispanic census tracts were more likely to exit assistance, but consumers in Majority Black census tracts were somewhat less likely to exit assistance than their counterparts in majority white census tracts. Mortgage borrowers in non-metro area census tracts, in counties with higher numbers of COVID-19 cases, and with higher unemployment rates were less likely to exit assistance. Meanwhile, consumers with higher credit scores and higher balances were both more likely to exit assistance when holding other factors constant, reflecting the likelihood that these consumers are well-off and consequently less affected by the COVID-19 income shocks.

What’s next?

The first post in this series showed that delinquencies have been low throughout the pandemic, and the high rates of payment assistance, as documented in this post, are likely at least partly responsible. As the assistance from programs such as the Federal CARES Act ends, the risk of reported delinquencies and even foreclosures may rise. To ensure a smooth and orderly transition out of the widespread payment assistance available during the pandemic, the Bureau recently finalized a rule establishing temporary special safeguards to help ensure that borrowers have time before foreclosure to explore their options, including loan modifications and selling their homes. In the next post in this series, we will examine trends in consumers’ use of credit cards during the pandemic.