Delinquencies on credit accounts continue to be low despite the pandemic

This post is the first in a series documenting trends in consumer credit outcomes during the COVID-19 pandemic. Last August, we published a report on early trends in consumer credit outcomes through June 2020, which found largely positive trends in those outcomes despite widespread economic hardship due to the pandemic. In this series we will examine how the trends in consumer credit outcomes have evolved since June 2020.

This post focuses on trends in delinquencies for auto loans, student loans, mortgages and credit cards. Possibly due to federal, state and local policy interventions providing payment assistance and income support, in the August 2020 report, we found that new delinquencies declined for auto loan, mortgage, student loan, and credit card accounts through June of 2020. Since July 2020, delinquencies for auto loans and credit cards have risen somewhat, but as of March 2021, the rate of new delinquencies on all four types of credit are still below pre-pandemic levels.

We use the Bureau’s Consumer Credit Panel (CCP), a deidentified sample of records from one of the three nationwide consumer reporting agencies. We focus on month-to-month transitions in delinquencies—loans that were reported as current in one month and delinquent the next, or were already delinquent and increased the number of days past due. The share of loans that became current or less delinquent was largely constant before and during the pandemic (not shown), and so we focus on transitions into delinquency. The August 2020 report contains additional details on the methodology.

New Delinquencies Remain Low and Have Not Returned to 2019 Levels

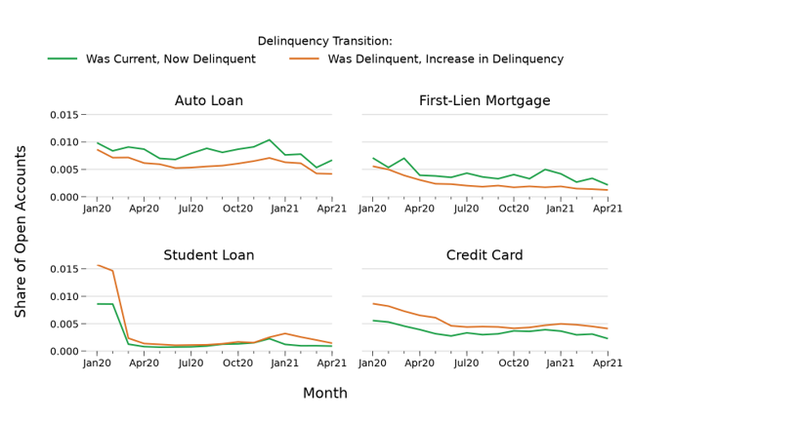

In the figure above, we plot the share of all open auto loan, mortgage, student loan and credit card accounts that transitioned to being delinquent in each month from being current in the previous month, and the share that transitioned from a lower level of delinquency to a higher level (e.g., from 30 days-past-due to 60 days-past-due). The figure focuses on the period from January 2020 to April 2021—the August report showed that rates of delinquency transitions were essentially flat or slightly increasing during 2019 and early 2020 for all four types of credit. As we documented in the August report, new delinquencies fell modestly between February 2020 and June 2020.

After June 2020, new delinquencies for auto loan and credit card accounts began to rise gradually, although by December 2020, the share of open accounts transitioning into delinquency was lower or approximately the same as it had been prior to the pandemic. New delinquencies for student loans also ticked up slightly since the summer of 2020, although the rate of delinquencies for these loans is still quite low, since a large share of student loans continue to be subject to automatic payment suspension under the CARES Act and administrative action by the Department of Education. Indeed, for student loans that do not appear to be receiving payment assistance, new delinquencies began rising in April of 2020 (not shown). New delinquencies on mortgages remained low from July 2020 through April 2021, likely reflecting the forbearances available under the CARES Act, which have since been extended through September 30, 2021 as of this writing.

Despite the increasing trend in delinquency transitions for auto loans and credit cards through the second half of 2020, new delinquencies declined slightly for all four types of credit between December 2020 and April 2021, possibly reflecting the effect of stimulus checks sent to many Americans around this time.

Recent Trends in Delinquencies Were More Pronounced for Sub-Prime Borrowers Compared to Borrowers with Higher Credit Scores

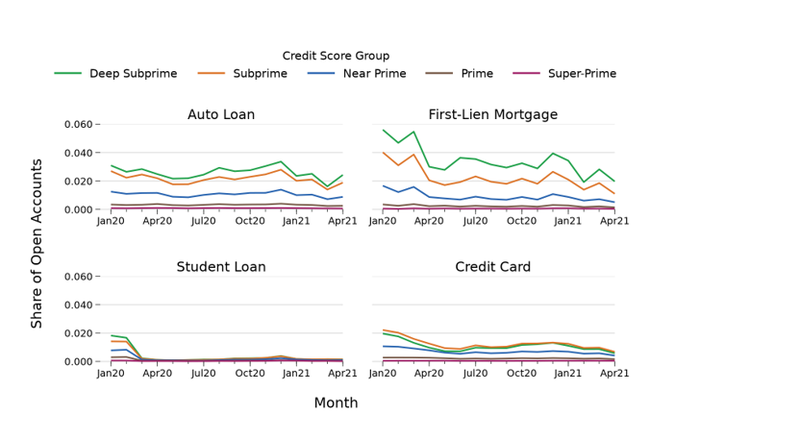

In the figure above we break out the share of accounts that transition into delinquency by credit score groups (see here for how Bureau researchers typically group consumers in the CCP by credit score). In the original August 2020 report we found that the decrease in new delinquencies through June 2020 was consistent across different groups of consumers, including consumers with high and low credit scores. Similarly, since June of 2020, the overall trends in new delinquencies were similar across credit score groups, although the trends were more pronounced for consumers with lower credit scores.

What’s next?

Additional stimulus payments of up to $1,400 per person were sent to many Americans in March and April 2021, which along with other benefits such as extended unemployment insurance may continue suppress delinquencies in the near term. Time will tell whether delinquencies begin to rise again through the summer and fall of 2021. As increasing vaccination rates bring COVID-19 cases down and local economies re-open, we may see the increased economic activity keep delinquency rates down. At the same time, many accounts that would be delinquent in the absence of the current assistance programs may begin to be reported as delinquent as that assistance ends. In a later post of this series we will discuss the trends in payment assistance since June 2020.