What are the signs of a student loan scam?

Scammers often make false claims and try to charge you for things you could do yourself for free. Protect yourself from student loan scams, including student loan forgiveness scams and student loan phone scams, by looking for warning signs.

According to enforcement actions taken by the CFPB, the Federal Trade Commission, and state attorneys general, scammers have stolen millions of dollars from student loan borrowers. Individual borrowers have lost hundreds, and, in some cases, thousands of dollars. Scammers often target distressed borrowers or people looking for help to manage their loans.

Some debt relief scammers run aggressive marketing practices to target vulnerable student loan borrowers. A person or business might be trying to scam you if they do any of the following:

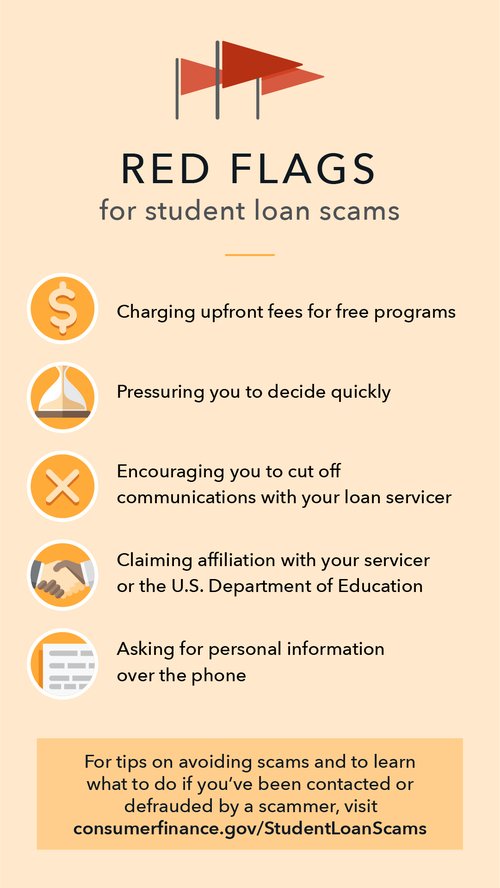

- Pressure you to pay up-front fees. Your student loan servicer will help you with your loans for free, so companies that request payment for debt relief services before providing help are breaking the law. These companies may even ask for your credit card number before they explain how they’ll help you. If a company requires you to pay an up-front fee or tries to make you sign a contract on the spot, it is likely a scam.

- Promise immediate student loan forgiveness or debt cancellation. Debt relief companies do not have the ability to negotiate with your creditors for a “special deal.” For borrowers with an income-driven payment plan, the amount they pay each month is set by federal law. For most borrowers, loan forgiveness is only available through programs that can require many years of qualifying payments or other qualifying criteria.

- Guarantee they can remove legally owed debts from your credit report. Credit repair and debt settlement companies cannot remove debts that you legally owe.

- Demand that you sign a “third party authorization.” A “third party authorization” or a “power of attorney” are written agreements giving a person or company legal permission to talk directly to your student loan servicer and make decisions on your behalf. In some cases, they may even step in and ask you to pay them directly, promising to pay your servicer each month when your bill comes due. Beware of any company that cuts off communication between you and your servicer. Make sure you’re involved in any communications with your servicer, as well as in the completion of any paperwork to change your repayment plan.

- Ask for your Federal Student Aid information. Your FSA ID is a unique username and password to access information about your federal student loans. If you give that information away, you are giving a person or company the power to perform actions on your student loan on your behalf. Do not provide your FSA ID to anyone. The Department of Education or your servicer will never ask for your FSA ID or password.

- Claim to be affiliated with the Department of Education or your student loan servicer. Scammers may try to appear legitimate by using official sounding names, logos, or websites. For federal student loans, if you want to consolidate your student loans or change repayment plans, the process should happen through one of the government’s official loan servicers or websites with “.gov” in their addresses.

Scammers sometimes unlawfully get personal information about you from your credit report. So even if a company claims to know your student loan balance or other details about your loans, they still may not be legitimate.

Despite what student loan debt relief companies may tell you, you NEVER have to pay someone else to contact your student loan servicer. If you’re struggling to repay your student loans, contact your servicer directly for help. You can change your repayment plan with your servicer for free. You can also work with your servicer to explore other payment relief options, including deferment, forbearance, and loan cancellation benefits. Be sure to learn about what’s available by contacting your servicer or through the CFPB’s Repay Student Debt tool.

There are also non-profit organizations that can help you figure out a plan to repay your debt. Non-profit credit counselors sometimes offer student loan coaching services. They will generally offer free budget analysis services to look at all your debts and may offer additional support to help you sort out your student loan options for a fee. Honest companies will never cut you off from communications with your servicer or require you to sign a contract without first providing an initial budget consultation.

What to do if you were defrauded by a student loan forgiveness scam

If you were targeted by a student loan forgiveness scam, you can report it to the Federal Trade Commission or your state’s attorney general. You can also alert your student loan servicer and instruct them to only provide information about your student loan directly to you.

Page last modified @