One thing you can do to take control of the homebuying process and save on your new home—in any housing market

Homebuying season is in full swing. If you’re a homebuyer or prospective homebuyer, it can feel like a bit of a rollercoaster at times, especially in the current market of rising home prices and a low inventory of homes for sale.

But, there’s one thing you can do to put yourself more in the driver’s seat—and it has the potential to save you real money on your home purchase: Shop for your mortgage.

Research from the Bureau's newly released Know Before You Owe: Mortgage shopping study found that homebuyers have gaps in their mortgage knowledge. But the research also found that just the process of shopping for a mortgage makes homebuyers more knowledgeable.

And shopping around for your mortgage has the potential to lead to real savings. It may not sound like much, but saving even a quarter of a point in interest on your mortgage saves you thousands of dollars over the life of your loan.

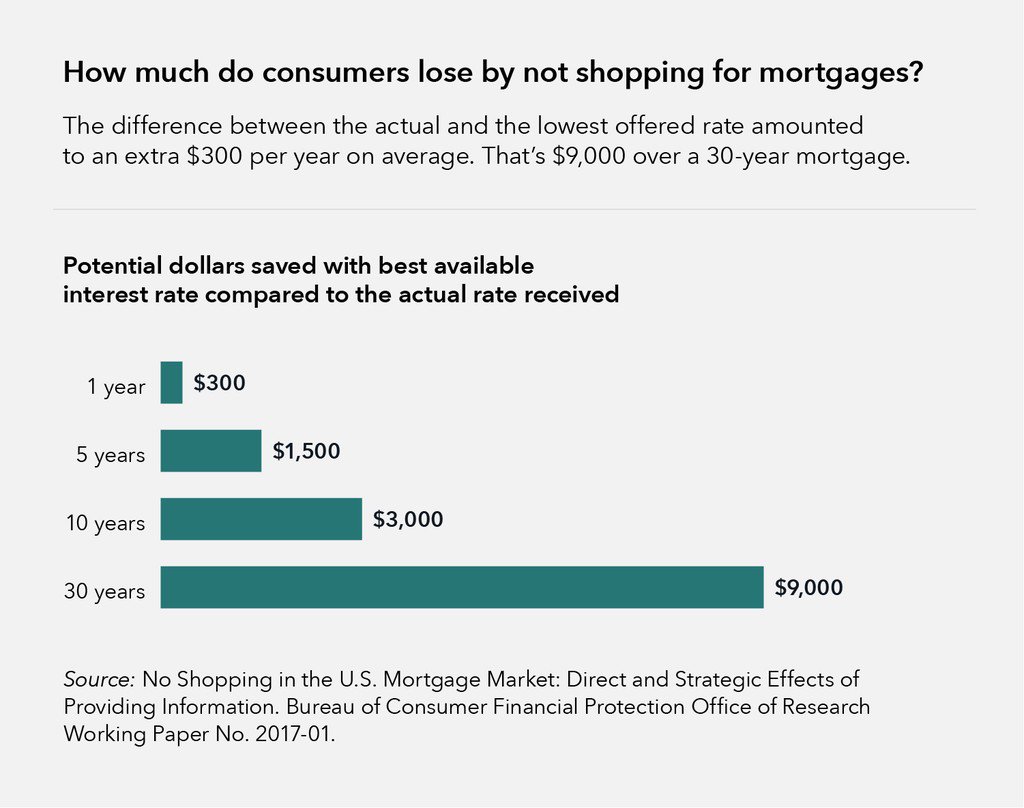

According to the Bureau's previously published paper, No shopping in the U.S. mortgage market: Direct and strategic effects of providing information , for the average person, the difference between the actual rate they got and the lowest offered mortgage rate available to them amounted to an extra $300 per year. That’s $9,000 over a 30-year mortgage. But close to half of all homebuyers don’t shop before taking out a mortgage.

There are a few possible reasons for this.

Rates change regularly, and it takes more than an online search to get reliable, up-to-date information. Also, getting an accurate rate quote generally requires sharing personal financial information, so homebuyers may be wary of sharing such information with several lenders.

Another reason people don’t shop around for their mortgage is because most believe it doesn’t make a difference. According to the National Survey of Mortgage Originations (NSMO), a joint project by the Bureau and Federal Housing Finance Agency (FHFA), most consumers think that “prices are roughly the same” across lenders.

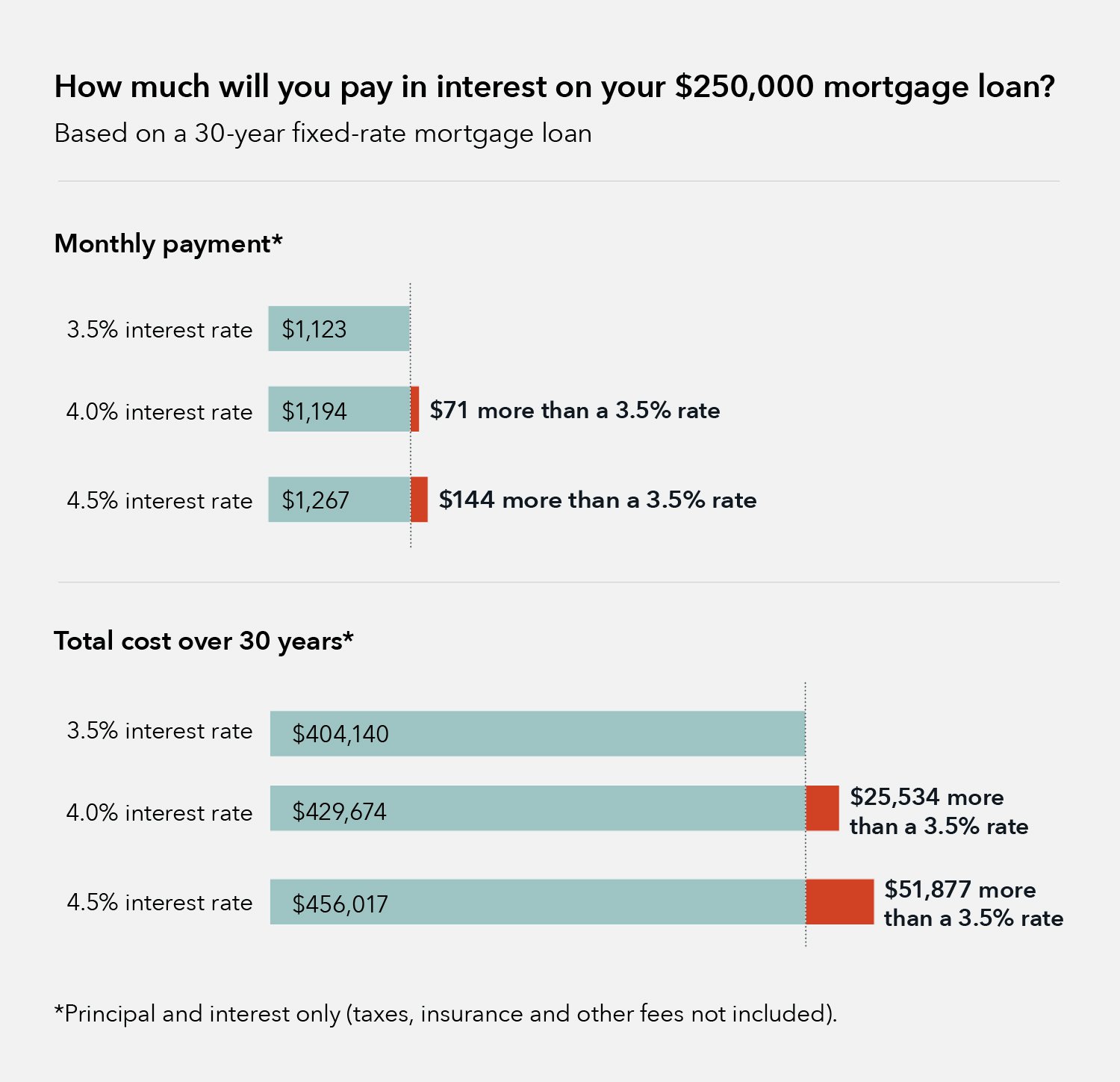

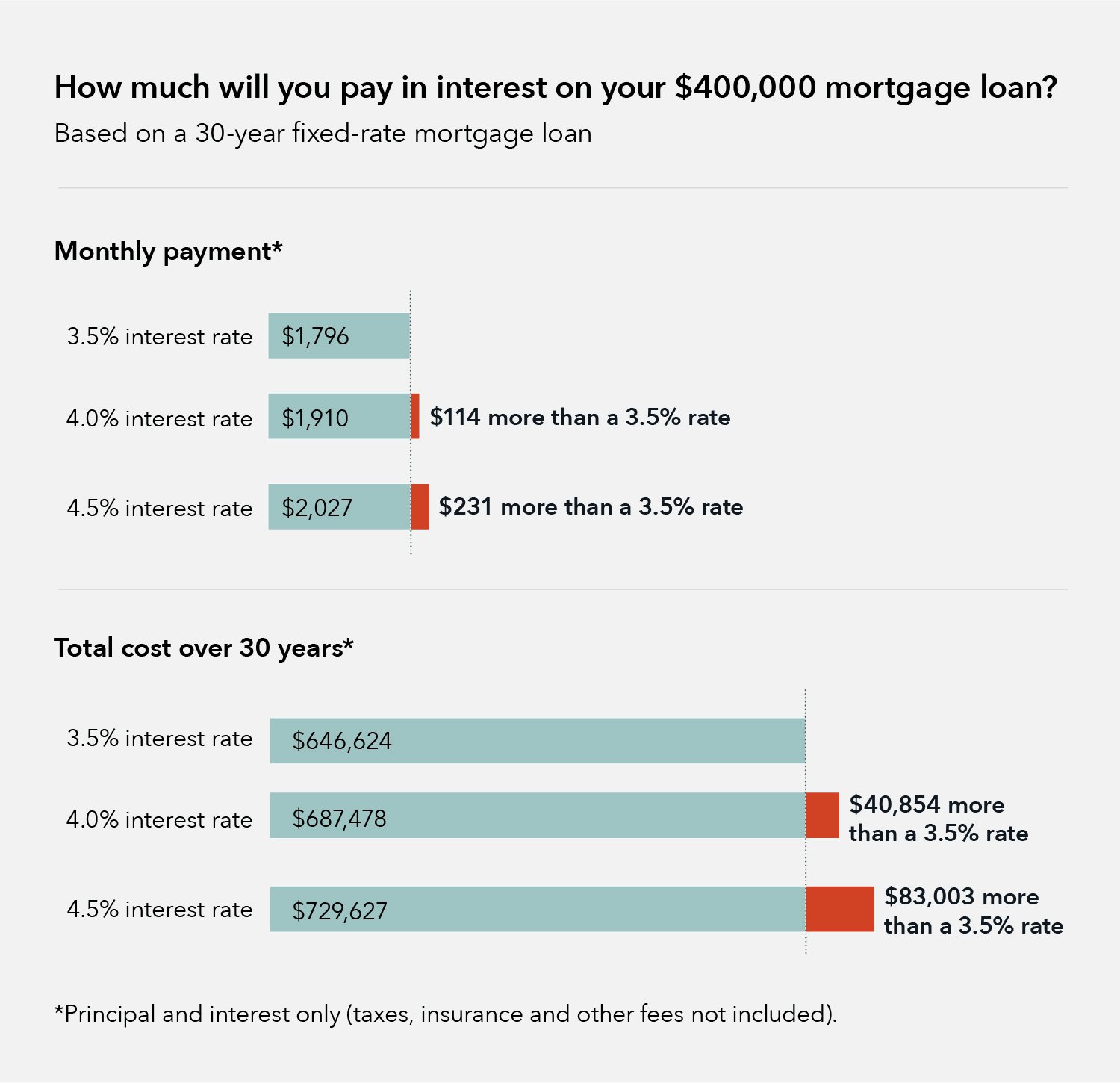

View infographics for interest paid on a $250,000 mortgage and a $400,000 mortgage.

{kind=link}

If the rates were more or less the same, it wouldn’t make sense to go through the hassle of talking to multiple lenders. But Bureau research shows that interest rates can vary by more than half of one percent, or 50 basis points in mortgage jargon, for similarly qualified borrowers looking for similar types of mortgage loans.

For example, in dollar terms, the difference between an interest rate of 3.5 percent and 4.0 percent on a $400,000 mortgage amounts to an extra $114 each month on a 30-year loan—for a $250,000 mortgage the difference is $71 each month on a 30-year loan.

Talking to multiple lenders and understanding all of the loan products and options available to you can help you find the best rate available to you and lead to significant savings.

What does this all mean for homebuyers?

There’s likely a range of mortgage interest rates available to you, and it can really pay off to shop around. The Bureau's Buying a House tools and resources can help you throughout your homebuying journey. To get the best interest rate you qualify for, here are a few things to consider:

- Talk to multiple lenders. With interest rates for similar loans varying by more than 50 basis points, talking to multiple lenders can give you a better idea of the rates available to you. Make sure to compare the overall terms and fees for each loan to understand the true cost of each loan you’re considering.

- Ask each lender about other loan products they sell that might be right for you. You may qualify for several different loans, and the rates and fees on each product are likely to vary.

- Consider taking a homebuying class or working with a housing counselor. A HUD-approved housing counseling agency can give you advice on buying a home and choosing the type of mortgage that’s right for you.

- Check your credit reports to make sure there aren’t any errors and to see what steps you can take to raise your credit scores.