Office of Research blog: Update on student loan borrowers during payment suspension

In April, we released a report on the credit health of student loan borrowers during the pandemic and identified the types of borrowers who may struggle when the federal payment suspension ends. Since that report was released, inflation has risen and delinquencies and balances have increased for consumers across credit products. These developments may signal or contribute to potential payment difficulties for borrowers going forward.

At the same time, the federal government extended the payment suspension through the end of 2022 and announced a new plan to provide one-time targeted student loan debt relief that would reduce the burden for many student loan borrowers and eliminate loans entirely for some borrowers. For borrowers with incomes under $125,000 individually ($250,000 for households), the plan would provide up to $20,000 in debt relief on federally held loans for Pell Grant recipients, and up to $10,000 in debt relief for other borrowers with federally held student loans.

In this post, we provide updated data showing that student loan borrowers are increasingly likely to struggle and may face difficulties once their monthly student loan payments are reinstated. We also show how student debt cancellation may substantially reduce the number of borrowers at risk when the payment suspension ends in January 2023.

Increasing rates of delinquency on non-student-loan credit

Using the CFPB’s Consumer Credit Panel (CCP), a deidentified sample of credit records from one of the nationwide consumer reporting agencies, we examine consumers who are expected to have scheduled loan payments at the end of the suspension, but we exclude consumers who have fully repaid their loans—or had their loans forgiven—since the last report.1 We also exclude borrowers with defaulted student loans since they will not have regular scheduled payments after the suspension ends if their loans are not rehabilitated. Many borrowers with defaulted loans, however, may have their loans canceled. For example, 39 percent of borrowers with a defaulted student loan on their credit record in the CCP have balances less than $10,000, and 23 percent have balances between $10,000 and $20,000.2

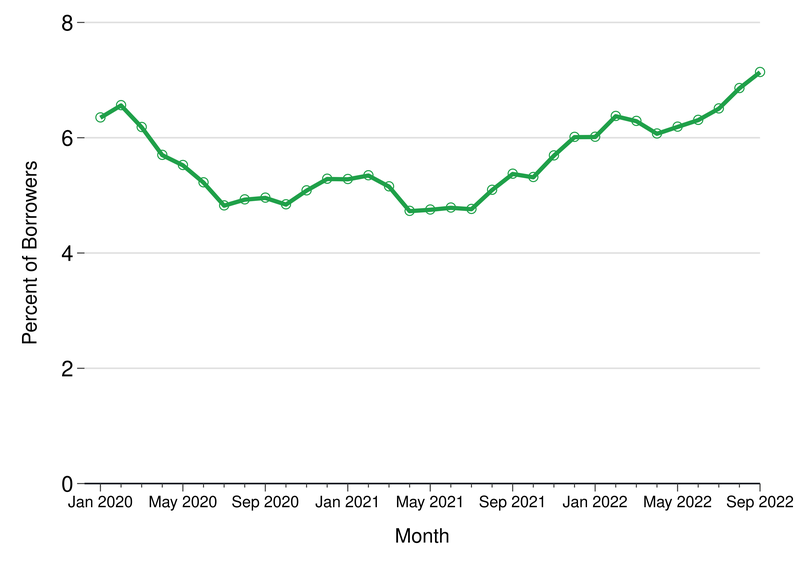

At the start of the pandemic, several policy interventions likely helped student loan borrowers avoid delinquencies on other credit products, but as those programs ended, delinquencies began to rise. The figure below shows that a growing share of student loan borrowers are 60 days or more past due on a non-student-loan credit account since mid-2021. As of September 2022, 7.1 percent of student loan borrowers who were not in default on their loans at the start of the pandemic were having difficulty repaying other debts, as compared to 6.2 percent of these borrowers at the start of the pandemic. Delinquency rates have risen even further for borrowers with defaulted student loans, increasing from 9.8 percent at the start of the pandemic to 12.5 percent as of September 2022 (not shown). If this rising delinquency trend doesn’t change, more borrowers may struggle as they face additional payments each month.

Figure: Percent of student loan borrowers in sample 60+ days delinquent on other credit products

Source: CFPB CCP.

While delinquencies have risen overall, many borrowers may have up to $10,000 (or $20,000) in balances canceled under the debt relief policy announced in August. While we can’t determine which borrowers are eligible for this relief, this new policy would very likely reduce the number of student loan borrowers in distress when the payment suspension ends.3 Borrowers with lower balances are somewhat less likely than those with higher balances to be behind on payments for other debts, but 25 percent of those with a non-student-loan delinquency have student loan balances of less than $10,000. An additional 19 percent of these borrowers have balances between $10,000 and $20,000. That is, many of the student loan borrowers who are currently struggling with repayment on other debts might no longer have student loan debt to repay when the payment suspension ends. As noted above, an even larger share of borrowers with defaulted student loans have balances under the debt cancellation thresholds. And many other eligible borrowers in distress may face lower monthly payments, even if they don’t enroll in an income-driven repayment plan, because of their reduced balances.

Monthly payments across credit products have increased

Not only has the share of student loan borrowers with delinquencies on other debts trended upward since mid-2021, but more student loan borrowers face higher monthly payments on non-student loans. In our earlier report, we found that, as of February 2022, 39 percent of student loan borrowers in our sample had scheduled monthly payments for all credit products—other than their student loans and mortgages—that increased 10 percent or more relative to the start of the pandemic.4 As seen in the table below, this has increased to 46 percent of student loan borrowers as of September 2022.

Auto loans, the highest balance-credit product after mortgages and student loans for many borrowers, drove much of the increase, but overall, there was a 15 percent increase in median monthly payments on non-student-loan debts for student loan borrowers in our sample since the start of the pandemic.5 While these higher payments may be manageable for borrowers who have seen their incomes grow over the pandemic, others may be falling behind, as suggested by the increase in delinquencies shown in the figure above.

Table: Payment and risk factor status for student loan (SL) borrowers, September 2022

| Borrower group | Active delinquency, Sep. 2022 (%) | Share with over 10% increase in scheduled non-SL, non-mortgage payments, Mar. 2020-Sep. 2022 (%) | Share with two or more risk factors (%) | Share (%) |

|---|---|---|---|---|

Overall |

7.1 |

46 |

17 |

100 |

Prior SL delinquency |

- |

- |

- |

- |

Never in repayment |

6.5 |

53 |

6 |

18 |

Delinquent |

14.7 |

44 |

72 |

7 |

Not delinquent |

6.6 |

45 |

14 |

75 |

Census tract income |

- |

- |

- |

- |

Low |

10.8 |

48 |

21 |

18 |

Moderate |

7.6 |

47 |

17 |

42 |

High |

5.0 |

45 |

14 |

40 |

Age |

- |

- |

- |

- |

18-29 |

5.5 |

54 |

13 |

33 |

30-49 |

8.7 |

46 |

20 |

47 |

50+ |

6.3 |

33 |

14 |

20 |

SL balances, Sep. 2022 |

- |

- |

- |

- |

Less than $10,000 |

7.0 |

44 |

12 |

26 |

$10,000-$19,999 |

7.1 |

46 |

14 |

19 |

$20,000-$34,999 |

6.7 |

48 |

15 |

19 |

$35,000-$49,999 |

7.7 |

47 |

19 |

11 |

$50,000 or more |

7.4 |

46 |

23 |

26 |

Note: All statistics are calculated for student loan borrowers who may have a payment due when the suspension ends and who had an outstanding student loan in February 2020. Scheduled payments include all minimum scheduled monthly payments for all credit products other than student loans and mortgages. Prior student loan delinquency is defined as having a student loan in February 2020 reported as 90 days or more past due while those classified as never in repayment have no reported prior payments as of February 2020. Census tract categories are defined by adults in the tract with household income below 200 percent of the Federal poverty threshold; “low” income is 40 percent or more of adults, “moderate” income is 20 percent or more but less than 40 percent of adults, and “high” income is less than 20 percent of adults. Source: CFPB CCP.

Increasing risks for many student loan borrowers may be alleviated by debt cancellation

In our April report, we also focused on five potential risk factors that indicate student loan borrowers might struggle when the payment suspension ends: pre-pandemic delinquencies on student loans, pre-pandemic payment assistance on student loans, multiple student loan servicers, delinquencies on other credit products since the start of the pandemic, and new non-medical collections during the pandemic.

Since that report, delinquencies on non-student-loan products have risen further, as discussed above. There has also been a small increase in the share of borrowers with new non-medical collections reported on their credit records (not shown). Overall, this has led to an increase in the number of borrowers with two or more risk factors from 5.1 million to 5.5 million student loan borrowers.

However, as many as one-third of borrowers with two or more risk factors may have their balances completely canceled. Specifically, 19 percent of these borrowers currently have balances under $10,000 and 16 percent have balances between $10,000 and $20,000 (not shown). So, despite worsening credit outcomes overall, the cancellation of some student loan debt means that fewer student loan borrowers are likely to be at risk of payment difficulties when federal student loan payments resume in January 2023 than they otherwise would be. And many borrowers with multiple risk factors who still have outstanding balances when payments resume may have reduced balances going forward.

In addition, at-risk borrowers with loans remaining after the debt cancellation may avoid payment difficulties by enrolling in an income-driven repayment plan . Currently many borrowers can qualify for plans that cap their monthly student loan payments at 10 percent of their discretionary income each month. A proposed new plan would lower that cap to 5 percent while also categorizing more income as non-discretionary. Prior to the pandemic, borrowers with larger balances were more likely to be enrolled in an income-driven repayment plan, so they may have more experience navigating the process. But they were also more likely to have a delinquent student loan or other credit product and would still have substantial loan balances even after any debt cancellation.

The Office of Research will continue to monitor how student loan borrowers are doing as scheduled payments resume and these new policies are rolled out.