Making the move to homeownership on your own or with someone else

Buying a home is exciting. It’s also one of the most important financial decisions you’ll make. Choosing a mortgage to pay for your new home is just as important as choosing the right home.

You have the right to control the process. Check out our other blogs on homebuying topics, and join the conversation on Facebook and Twitter using #ShopMortgage.

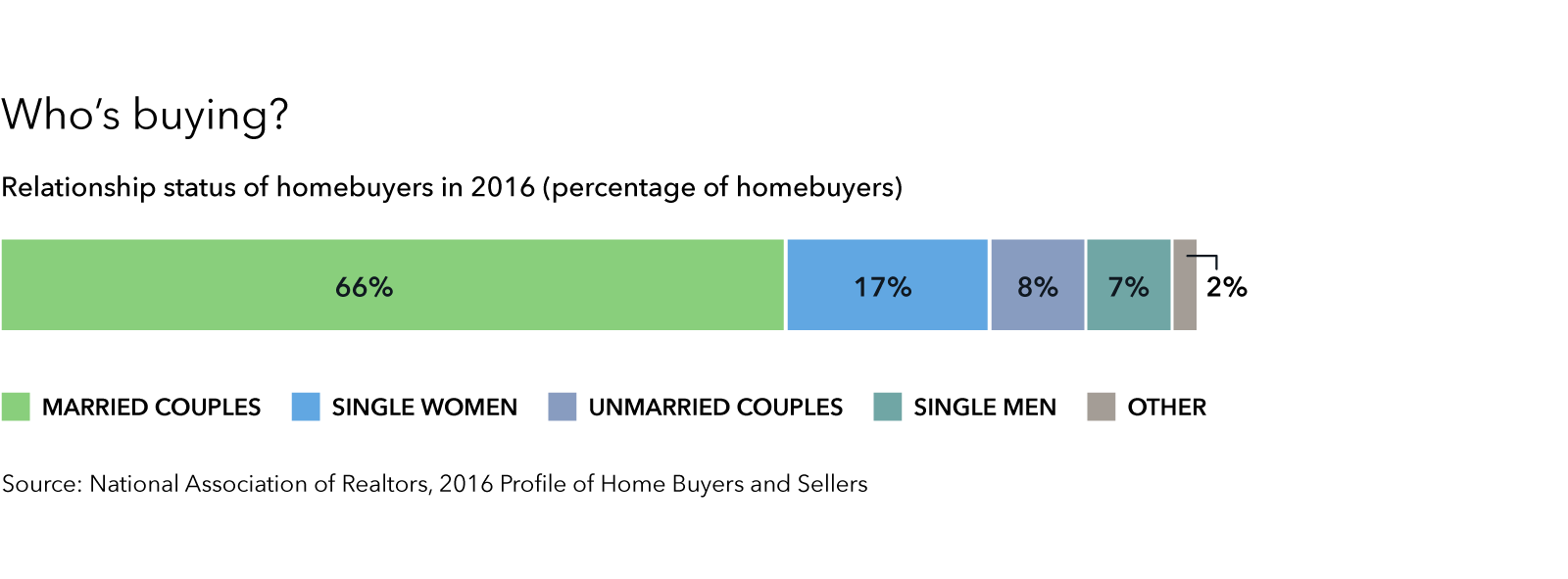

Three decades ago, over 80 percent of homebuyers were married. In 2016, only 66 percent were married. While married couples continue to make up the largest share of homebuyers, the share of single women buying homes has risen significantly since the mid-'80s. According to one national survey, in 2016 single women represented 17 percent of total home purchases, compared to 8 percent for unmarried couples and 7 percent for single men. No matter your relationship status, we can help make buying a home and shopping for a mortgage less complicated.

Whether you’re looking to buy a home by yourself or with someone else, it pays to do your homework, know what you’re getting into, and shop around for a mortgage.

Keep reading to learn about:

- Shopping for a mortgage on your own

- Shopping for a mortgage with your spouse or significant other

- Shopping for a mortgage on your own when you’re in a relationship

- Steps all homebuyers should take when buying a home

Shopping for a mortgage on your own

If you’re single and want to buy a home, you’re not alone. The CFPB’s nationally representative survey of mortgage borrowers found that in 2013, 23 percent of homebuyers were single. When you are shopping for a mortgage, it’s important to know that lenders cannot discriminate against you based on your marital status. If you have enough money for a down payment, enough income to support the monthly payments, and if you meet the other eligibility criteria (credit history, the amount of debt you have compared to your income, etc.), then you can qualify for a mortgage as a single person.

If you’re recently divorced, you may need to do some work first to make sure that your finances are fully separated from your former spouse. For example, if you previously owned a home with a former spouse, make sure that the old mortgage has been paid off. If the home was sold, make sure that the mortgage was paid off at closing. If your former spouse kept the home, make sure that the mortgage has been refinanced to remove your name. If your credit report shows that you are still legally responsible for the old mortgage, it may be difficult to qualify for a new mortgage in your own name. Checking your credit report is a good way to see whether old joint accounts are still active.

Shopping for a mortgage with your spouse or significant other

In some ways, shopping for a mortgage with someone else is the same regardless of whether you and the other person are married, registered domestic partners, unmarried partners, or just friends. Lenders cannot discriminate against you based on your marital status. However, there are different things to consider depending on who you are getting a mortgage with—particularly when it comes to the real estate title and the tax implications. Here are some things to consider:

Understand how your mortgage application will be considered

If you apply for a mortgage jointly with someone else, whether you are married or not, lenders evaluate your mortgage application as co-borrowers. Collectively, you’ll need to have enough income to make the payments and demonstrate that you’ll be able to make payments in the future. If one person doesn’t have an income or doesn’t have much income, that’s okay as long as the other person has enough.

Lenders typically use the credit scores of the person with the lowest credit scores to evaluate the mortgage application. If one person has a low credit score, you can apply for the mortgage without that person, but then the lender typically won’t consider that person’s income.

Talk about how you will share the responsibilities of the mortgage

When you buy a home together, you and your co-borrower are jointly responsible for paying the mortgage. Each of you is on the hook to pay the whole amount, even if you have a different agreement between yourselves. If you agree to split the payment 50/50, but one person is short on money one month, the other person will have to cover the difference. If they don’t, the payment will be recorded as incomplete, and the credit of both borrowers may suffer.

There are many ways to manage your financial responsibilities, no matter what your relationship. What’s important is that you talk about it in advance and have the same expectations. Here are some questions to start your conversation:

Questions to consider

- Are your credit scores about the same or significantly different? Check your credit reports and scores together.

- Who will contribute how much to the down payment? Will you split it 50/50 or some other arrangement?

- How will you share the monthly mortgage payment? Will you split it 50/50, or some other arrangement?

- How will you manage the logistics of pooling income to make the monthly payment? Will you have a joint checking account, or some other arrangement?

- Who will be responsible for making sure the payment is made on time each month?

- How will you manage payments for taxes and insurance if those expenses are not included in an escrow account?

- How will you manage the expenses of home maintenance? Will you have a joint savings account, or some other arrangement?

It’s important to write down your answers to these questions, so everyone remembers the agreement the same way. If you are buying a home with someone other than your spouse, it’s a good idea to get a lawyer to help you draw up a simple contract that clearly spells out each person’s responsibility and what happens if someone fails to live up to their responsibility.

Understand what will happen if one person wants to move out someday

There’s one big difference between buying and financing a home with a spouse versus someone you’re not married to. If you’re married and one day you split up, you and your spouse will have to figure out what to do about the home and the mortgage as part of the divorce, or a court will decide for you.

If you’re not married, there’s no divorce process. You’ll still own a home together—and are still responsible for the mortgage together—until you do something to legally change that. Of course, it’s hard to know now exactly how you would want to resolve things in the event that one of you wants to move out one day. A lot will depend on your personal and financial circumstances at the time. But it’s important to think about and agree in advance how you will decide what to do if you were to part ways. Consider contacting a lawyer to help you write a contract that specifies what the options are and who has what responsibilities. The contract can also specify how you will resolve problems.

No matter what, it’s important to at least understand your options. Here are a few common ways people deal with the situation when co-borrowers want to part ways:

Sell the home

You put the home up for sale and everyone moves out. Until the home is sold and the mortgage is paid off, you and your co-borrower are still jointly responsible for making the mortgage payments on time each month. Once the home is sold, the proceeds will go first to pay off the mortgage; any remaining proceeds are divided and everyone goes their separate ways. If you are unable to sell the home for at least as much as the mortgage, you and your co-borrower may not be able to sell the home at all.

One person moves out and lets the other borrower keep the home

If one co-borrower wants to keep the home, the one who wants to leave can sign over their ownership share to the remaining borrower. This is particularly common as part of a divorce settlement or separation agreement. If there is equity in the home, the person who is staying may need to “buy out” the person leaving. In this situation, the person who wants to stay pays cash to the person who wants to leave in exchange for their share of the ownership.

Signing over the ownership of the home doesn’t change the joint responsibility for the mortgage. Here are some considerations to keep in mind:

- The remaining borrower should refinance the mortgage in their name only. If they can’t qualify for and afford the mortgage on their own, the best solution is usually to sell the home. If the amount still owed on the mortgage is close to or more than the value of the home, it may not be possible for the remaining borrower to refinance the loan.

- If the remaining borrower doesn’t refinance, both borrowers’ credit could suffer if the mortgage payments are not made on time.

- It may be difficult for the person who leaves to get a new mortgage while their credit reports show that they are still responsible for the old mortgage.

It’s important to keep in mind that home prices don’t always go up. If the value of the home goes down, the home may become “underwater,” meaning that the home value is less than the amount owed on the mortgage. In this situation, it may be impossible either to sell the home or for one borrower to refinance. If one borrower moves out without a change in the loan, both borrowers are still legally responsible for the mortgage. If the person staying doesn’t make the payments, the home could go into foreclosure, which would affect the credit history of both borrowers.

Be aware of the types of ownership available in your state and consider getting legal advice

When you buy a home with someone else, the legal owners will be listed on the title, deed, or ownership documents. Depending on your state law, there are several different ways that property can be titled. The type of title defines the ownership rights in a home, for example, what happens when someone dies, or wants to sell or transfer their ownership share. The type of title can also define who can make decisions about the property, such as taking out a home equity loan.

Keep in mind that property, marriage, and inheritance laws differ widely from state to state. Your rights and responsibilities also change depending on how the property is owned and titled. Not all states offer all kinds of titles or define them in the same way. Depending on the state, some types of titles may have different implications based on whether you are married or not. Some states, known as “community property states,” have special rules for married couples.

The following information about titles is provided to give you a very basic idea of the types of ownership. It is not intended as a substitute for legal advice. Laws vary from state to state. Consider consulting with a real estate lawyer for advice on your specific situation. It’s important to make sure that you understand the benefits and drawbacks of the ownership and title options available in your state.

Joint tenancy with right of survivorship

This type of title is the most common choice among married couples, but you do not have to be related to use joint tenancy with right of survivorship. The ownership of the property is equally divided among the co-owners. In the event of one owner’s death, their share of ownership automatically passes to the other owner.

Tenancy by the entirety

This type of title is typically available only for married couples (and, in some states, civil unions or registered domestic partners). It is similar to joint tenancy with right of survivorship, but has additional restrictions and protections. Neither spouse can sell, transfer, or take out a mortgage on the property without the other spouse’s consent. Tenancy by the entirety is not available in all states.

Tenancy in common

This type of title allows you to decide how much of the property is owned by each person. For example, it could be 50-50 or you could own 70 percent of the home while the other person owns 30 percent. Each owner can sell or transfer their ownership share. If one owner dies, their ownership share will be distributed according to their will or state inheritance laws.

Shopping for a mortgage on your own, even when you’re together

Relationships can be complicated, and there are many ways to manage finances as a couple, regardless of whether you’re married. Some couples choose to join their finances completely, others choose to keep them completely separate, and many more choose a hybrid. Just because you’re together doesn’t mean that you have to buy a home together if it doesn’t make sense for you.

Some people may be in a relationship and ready to buy a home, but not ready to buy a home with their partner. Perhaps the partner is not financially ready to buy, or perhaps you have other reasons why buying a home together might not be a good idea. If you’re in this situation, you can consider buying a home on your own while maintaining your relationship. You and your partner can decide who will live in the home and pay toward the mortgage—but if the home and the mortgage loan are in your name, they are your financial responsibility.

Married people can also get a mortgage and own property in one person’s name only, if that makes sense for them. Of course, if you want to get a mortgage in your name only, you’ll have to be able to qualify for the mortgage on your own, using only your income and credit history. Lenders are not allowed to discriminate against applicants because they are married but want to get a mortgage on their own. However, if you live in a “community property state,” the property may be presumed to belong to both you and your spouse, even if the mortgage and title are in your name only.

It may be possible to put a spouse or partner’s name on the deed or title to the home, even if the mortgage is in your name only. However, there are risks that you should carefully consider and you may want to consult a real estate lawyer. For example, the other person could have ownership rights to the home, including the ability to take out a loan on the property or sell their share of the home independently (depending on the type of ownership).

If you’re considering buying on your own while in a relationship, it’s just as important to have a frank conversation with your partner about expectations as it would be if you were buying a home together. Here are some questions to start your conversation:

Questions to consider

- Will your partner help pay the monthly mortgage payments, or will that be your responsibility alone?

- Would you be able to handle the mortgage payments on your own for at least a few months, if you needed to?

- If you break up, what will happen? Will your partner simply pack their bags and move out? Will you owe any money to your partner for their contributions to the payments/home?

- If your home value increases, will your partner receive a share of that appreciation if you break up or decide to sell the home?

Just as when you’re buying together, it’s a good idea to write down your answers to these questions, and you may want to put those answers in a formal agreement. That way everyone remembers and is accountable to the agreement in the same way. You may want to talk with a real estate lawyer to make sure you understand exactly how the laws in your state work. A lawyer can also help you draw up a written agreement that clearly spells out who is contributing what and how things will be resolved if you decide to split up down the road. Legal advice and a written agreement can help to protect you and your partner.

Similarly, if your spouse or partner is considering buying a home on their own, it’s important to understand the risks for you, as the spouse or partner whose name is not on the title. If you are the person whose name is not on the title and you don't live in a community property state, you will have fewer rights to the property. If you’re not married, you may have no rights to the property. If your partner decides to sell the home, or loses it to foreclosure, you will likely have to move. It’s a good idea to have an honest conversation with your partner about expectations and consider consulting a real estate lawyer to understand your rights.

What everyone should know

Regardless of your relationship status, shopping for a mortgage for your first home can feel intimidating. We’ve got you covered. Our "Buying a House" tools will walk you through the steps, from creating a spending tracker to closing on your new home.

If you’re thinking about becoming a homeowner this year, we recommend checking your credit as soon as possible. This is the first step toward building a strong financial foundation for your home. If you’re buying with someone else, check your credit and review the reports together. We have information and tips to help you request copies of your credit reports, review them for errors, and find out your credit scores.

Before you begin shopping for your new home, we also recommend taking time to track your current spending and budgeting for your down payment and other expenses. It’s crucial to review your finances so that you know how much home you can afford. And for couples, reviewing your finances together is a great way to avoid any surprises and make sure you are both on the same page with your budget and financial goals. Take a look at our tools to help you track your current spending, determine an affordable down payment, and plan a budget.

Our interactive "Buying a House" tools can guide you through the entire home buying process, from preparing to shop to getting ready to close on your new home. Because choosing the right home loan is just as important as choosing the right home, we have information and resources to help you understand and compare loan offers.

We’ve got a lot of information on our site already to help you get started.

- Visit "Buying a House" to help you navigate the process all the way to closing.

- Check out Ask CFPB, our database of common financial questions.

- Ask us questions. We’ll feature some of the most frequently asked questions on our blog this spring.