Data Spotlight: Trends in discount points amid rising interest rates

The 2022 and 2023 housing market was marked by increasing affordability challenges for prospective homebuyers as rapidly rising interest rates reached a peak of 7.79 percent by October of 2023.1 Concurrent with rising interest rates, a larger share of borrowers paid discount points.

In this spotlight, we use quarterly data collected pursuant to the Home Mortgage Disclosure Act (HMDA) to look at the borrower and loan characteristics of homeowners that paid discount points between the first quarter of 2019 and the third quarter of 2023, a period that included record-high mortgage interest rates and preceded the Federal Reserve’s announcement of its intention to lower interest rates. We find that:

- The majority of recent borrowers paid discount points, including nearly 9 out of 10 borrowers with cash out refinances.

- More borrowers paid discount points as interest rates increased.

- Borrowers with lower credit scores were more likely to pay discount points.

The Consumer Financial Protection Bureau (CFPB) is monitoring increases in borrowers paying discount points, as well as increases to the amount borrowers are paying in points. Discount points may provide advantages to some borrowers, but the financial tradeoffs involved in discount points are complex, creating risks for consumers.

Discount points

Discount points are a one-time fee paid at closing to a lender in exchange for a lower interest rate. Paying one discount point is the equivalent of paying a fee of one percent of the loan amount, but discount points have no fixed value in terms of the change in interest rate. For example, a borrower with a $400,000 loan might have to pay one discount point ($4,000) to reduce their interest rate by 0.25%, but another lender might equate one discount point, at the same cost, with a higher or lower interest rate reduction. Similarly, interest rates offered by different lenders with or without discount points may also vary. For example, a lender may offer an interest rate of 7.0% without any discount points, while another lender may offer that same rate with one discount point. Discount points are typically paid by the borrower, but they can be paid by the home seller or a third-party, such as a homebuilder.

Lenders’ advertisements and initial price quotes to consumers often include discount points in the fine print, which can make their interest rates appear more competitive. Although discount points and APR are disclosed in advertisements and later in the Loan Estimate and Closing Disclosure, consumers who don’t understand the mechanics of discounts points could mistakenly believe a lender’s interest rate is a better deal than it is. Since discount points add an additional layer of complexity, borrowers would need to get offers from multiple lenders that have either the same interest rate or the same amount of discount points to tell which offer is the better deal for their situation. Choosing a loan based only on the interest rate can lead borrowers to pay for more discount points (sometimes unwittingly) than is optimal for their situation.

Even when consumers understand how discount points work, most borrowers only benefit from discount points if they keep their mortgage long enough that the cumulative monthly savings from the reduced interest rate outweigh the upfront costs. This is often referred to as keeping the mortgage past the “break-even period,” which can be roughly estimated by dividing the cost of the discount points by the borrower’s monthly savings. Borrowers who plan to keep their mortgage for a long time and have cash on hand may find it advantageous to pay discount points. However, discount points are less useful for cash-strapped borrowers and those who expect to refinance or move in the near future. Additionally, the historically high interest rate environment of the last year may prompt a higher share of borrowers to consider paying discount points to manage their monthly payments, especially when comparing it to the low interest rate environment that encompassed 2020 and 2021.

Data and methodology

Discount points is one of the data points collected and reported under HMDA. Lenders report the total amount that was paid, in dollars, to reduce the interest rate in the “discount points” data point. However, HMDA does not include how much the borrower’s interest rate is reduced based on the discount points paid or how much borrowers understand about discount points as a means of lowering their rate. In this data spotlight, we consider borrowers as having paid discount points if they paid at least an eighth of a point, or 0.125 percent of the loan balance, in discount points.

HMDA is a data collection, reporting, and disclosure statute enacted by Congress in 1975, which requires financial institutions to report application-level information about mortgages. HMDA data are the most comprehensive source of publicly available information on the U.S. mortgage market. In addition to submitting annual application-level data, the largest mortgage lenders must submit quarterly HMDA data to their regulators. Aggregate statistics from the quarterly data are publicly available in the HMDA quarterly graphs.

In 2023, 43 financial institutions submitted HMDA quarterly data. These institutions accounted for about 58 percent of the application/loan counts in 2022, despite representing only a small portion of the 4,451 financial institutions that reported HMDA annual data in 2022.

For the purposes of this data spotlight, we combined the quarterly data of the HMDA filers for 2023 with their annual HMDA data from 2019 through 2022, limiting our analysis to include closed-end, first-lien, 30-year mortgages for owner-occupied, site-built, one-to-four family homes, excluding reverse mortgages.

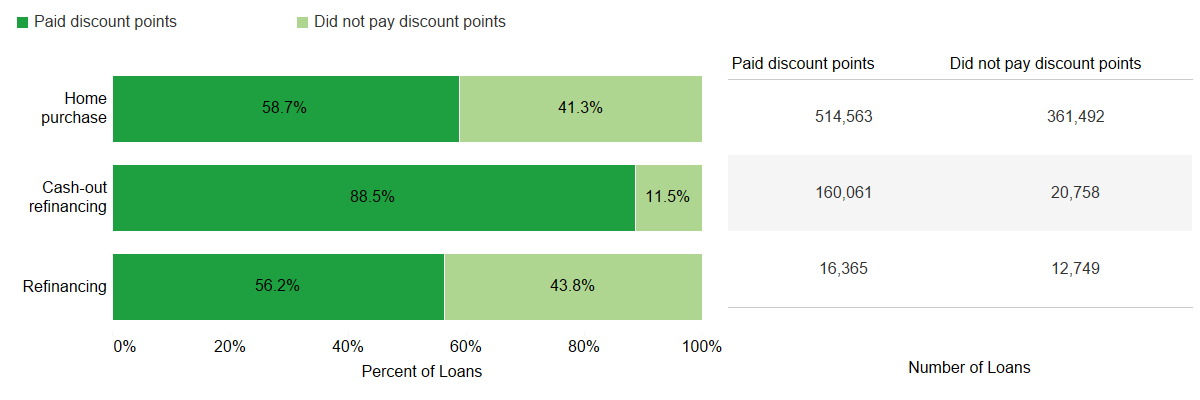

The majority of recent borrowers paid discount points, especially when getting cash out

Most consumers who got a mortgage in the first three quarters of 2023 paid some amount of discount points. Discount points were most common among borrowers with cash-out refinances, with nearly 9 out of 10 of those borrowers paying discount points. Additionally, 58.7 percent of borrowers with home purchase loans and 56.2 percent of borrowers with non-cash-out refinance loans paid discount points, as shown in Figure 1.

FIGURE 1: Volume of loans with discount points by loan purpose, Jan – Sep 2023

Source: HMDA quarterly data for 2023.

Borrowers with cash-out refinances also bought a larger number of discount points. The median amount of discount points (among borrowers who got them) was 2.1 points for cash-out refinance loans, 1.1 points for non-cash-out refinances, and 1.0 point for home purchase loans.

Even amidst the high interest rate environment, almost 200,000 borrowers in the 2023 quarterly data used cash-out refinances to tap their home equity. These borrowers may be cash-strapped and looking for ways to pay bills or other debts, which was the most popular use for funds from cash-out refinances from 2014 to 2020, according to the National Survey of Mortgage Originators .2

Borrowers with cash-out refinances may be more likely to pay discount points or be offered them by default because they have a ready source of liquidity: they can use the cash they would have gotten from their home equity to pay for the discount points. In contrast, borrowers with home purchase and non-cash-out loans typically have to pay for discount points out of pocket if they exceed the limit on how much of the closing costs (including discount points) can be rolled into the loan. Discount points can complicate the already-complex choice for homeowners to pursue cash-out refinancing over other sources of liquidity.

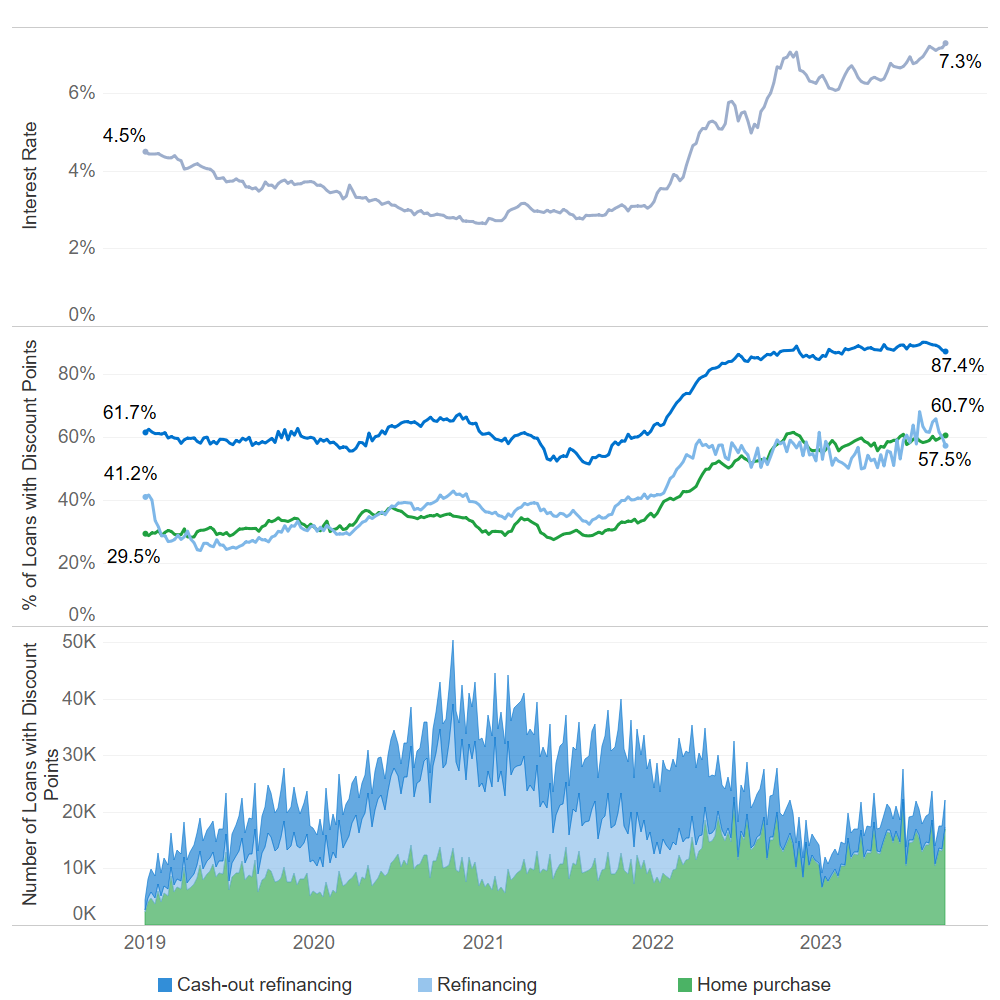

More borrowers paid discount points as interest rates rose

Across loan purpose categories, borrowers were more likely to pay discount points during periods where interest rates were high. For example, when interest rates on 30-year mortgages hovered at 2.6 percent in January of 2021, only 61.2 percent of cash-out refinance borrowers paid discount points. By the end of September 2023, interest rates had reached as much as 7.3 percent, and the share of cash-out refinance borrowers that paid discount points had increased to 87.4 percent. The same pattern follows for home purchase and refinance borrowers, which saw the share of borrowers that paid discount points jump from 30.5 percent and 36.4 percent in 2021 to 60.7 percent and 57.5 percent in 2023, respectively.

FIGURE 2: Mortgage interest rates, share of loans with discount points, and loan volumes, Jan 2019 – Sep 2023

Source: HMDA quarterly and annual data, Freddie Mac Primary Mortgage Market Survey .

The increase in the share of borrowers that paid discount points likely contributed to the rise in total loan costs, another data point collected under HMDA, seen in 2022.3 The total loan costs reported in HMDA include the origination fees charged by the lender, fees for services the borrower cannot shop around for (e.g., credit report fees), fees for services the borrower can shop around for (e.g., title insurance), and discount points paid. The median total loan costs for home purchase loans jumped by 21.8 percent between 2021 and 2022, while the median total loan costs for refinance loans increased by 49.3 percent.

As interest rates rose, more borrowers paid discount points. Industry participants have anecdotally noted that some consumers had anchored their expectations around the historically low rates from earlier years and were more willing to pay upfront costs to get a lower interest rate. It may also reflect borrower expectations that interest rates would remain high. Fannie Mae’s National Housing Survey suggests that, throughout most of 2023, consumers believed mortgage interest rates would continue to rise over the next year.4 Additionally, some lenders may have included discount points to maintain the interest rate borrowers received when they were offered prequalification for the mortgage in order to remain qualified, or to incentivize borrowers with lower interest rates.

However, research by Freddie Mac shows the interest rate differential between prime, conventional borrowers that paid discount points and those that did not pay discount points between 2018 and 2023 was minor, suggesting that paying discount points may not be the optimal option for consumers, though the analysis did not fully control for borrower and loan attributes.5

Discount points also play a role for investors who hold mortgage debt. When interest rates are falling or are expected to fall, investors face a high prepayment risk because consumers are likely to refinance and pay off their mortgage early (prepay). Therefore, even though an investor would benefit from a high interest rate, they know the cash flows could be short lived. Discount points can reduce the prepayment risk on a loan by lowering a consumer’s interest rate and thereby lowering their incentive to refinance. However, HMDA data do not include data on how much the borrower’s interest rate is reduced based on the discount points paid, making it difficult to analyze the likely magnitude or impact of these dynamics.

Homebuyers with lower credit scores were more likely to pay discount points

Homebuyers with low credit scores tended to pay discount points more often than borrowers with high scores, though trends vary across mortgage type. Overall, about 65 percent of homebuyers with Federal Housing Administration (FHA) loans paid discount points, compared to 62 percent for Department of Veterans Affairs (VA) loans and 57 percent for conventional loans. FHA and VA loans typically serve as alternative affordable options to conventional mortgages for homebuyers.

Figure 3 shows the share of home purchase borrowers that paid discount points, by loan type and credit score, in 2023. The borrowers who were least likely to pay discount points were conventional and VA homebuyers with credit scores of 800 or more. Yet even among these super-prime borrowers, slightly more than half paid discount points.

Meanwhile, discount points were especially prevalent among FHA homebuyers with low credit scores. FHA loans serve a large segment of the first-time homebuying population, likely a result of its product features, including its low-down payment options.6 As of 2023, about 4 out of every 5 FHA borrowers were first-time homebuyers.7 While we might not expect such a large share of FHA borrowers, a majority of which are first-time homebuyers, to have the funds available to pay a higher amount of closing costs, nearly two-thirds (65 percent) of FHA borrowers paid discount points. Usage of discount points is sharply higher for consumers with credit scores below 640, which is also the score range where it can become more difficult to qualify for FHA loans because lenders start to impose additional underwriting requirements.

FIGURE 3: Credit scores of home purchase loans with discount points, by loan type, 2023

Source: HMDA quarterly data from 2023.

It's possible lenders are offering these borrowers mortgages with discount points to ensure they qualify for a mortgage by lowering their monthly mortgage payments. As mentioned earlier, paying discount points can lower the interest rate on a mortgage and therefore the monthly payments for the life of the loan. Lenders may be attempting to lower the monthly payments and therefore the DTI so borrowers qualify for a mortgage. While most first-time homebuyers may be cash-strapped, many may look for alternative ways to finance their closing costs, like soliciting the financial help of family or friends to help pay discount points or negotiating for the seller to pay them.

In summary, 2022 and 2023 were marked by record-breaking interest rates that forced borrowers to quickly adapt. As a result, borrowers were more likely to pay discount points, with cash-out refinance borrowers the most likely to pay discount points as compared to other borrowers, and more likely to pay more discount points. In addition to adapting to the high interest rate environment, many lenders may also be using discount points to ensure that borrowers qualify for a mortgage. Borrowers with lower credit scores were more likely than those with higher credit scores to pay discount points, with discount points the most prevalent among FHA borrowers with low credit scores. This indicates that lenders may be using discount points to lower monthly payments and therefore debt-to-income ratio, one of the measurements lenders use to assess a borrower’s ability to repay, to qualify for a mortgage.

Analysis of HMDA data shows a rising share of borrowers are relying on discount points to lower their mortgage interest rate or to qualify for a mortgage. As discount points have become a more common part of the market, it becomes more important to understand the factors driving the increase in discount points and how borrowers end up paying for them.

Endnotes

-

Freddie Mac. Primary Mortgage Market Survey (Last Accessed December 2023), available at https://www.freddiemac.com/pmms .

↩ -

National Mortgage Database, National Survey of Mortgage Originations Public Use File Select Weighted Tabulations, 2013 - 2020, Table 29 (March 2023), https://www.fhfa.gov/DataTools/Downloads/Documents/NSMO-Public-Use-Files/NSMO-Select-Weighted-Tabulations-20230303.pdf.

↩ -

Consumer Financial Protection Bureau, Data Point: 2022 Mortgage Market Activity and Trends (2023), https://www.consumerfinance.gov/data-research/research-reports/data-point-2022-mortgage-market-activity-trends/.

↩ -

Fannie Mae, Consumer Optimism About Mortgage Rates Jumps Significantly (January 2024), https://www.fanniemae.com/newsroom/fannie-mae-news/consumer-optimism-about-mortgage-rates-jumps-significantly ; Fannie Mae, National Housing Survey (December 2023), https://www.fanniemae.com/media/50046/display .

↩ -

Freddie Mac. Economic, Housing and Mortgage Market Outlook – January 2024 (January 2024), https://www.freddiemac.com/research/forecast/20240122-us-economy-continues-expand .

↩ -

U.S. Department of Housing and Urban Development, Annual Report to Congress Regarding the Financial Status of the Federal Housing Administration Mutual Mortgage Insurance Fund, page 9 (2023), https://www.hud.gov/sites/dfiles/PA/documents/2023FHAAnnualReportMMIFund.pdf .

↩ -

U.S. Department of Housing and Urban Development, Annual Report to Congress Regarding the Financial Status of the Federal Housing Administration Mutual Mortgage Insurance Fund, page 9 (2023), https://www.hud.gov/sites/dfiles/PA/documents/2023FHAAnnualReportMMIFund.pdf .

↩

Page last modified @