What should I do if I can’t pay a medical bill?

Navigating the complexities of medical billing systems is extremely difficult. Make sure the provider accurately calculated the bill and that you owe it before you pay. There also may be protections under federal and state law as well as financial assistance that you may be entitled to claim.

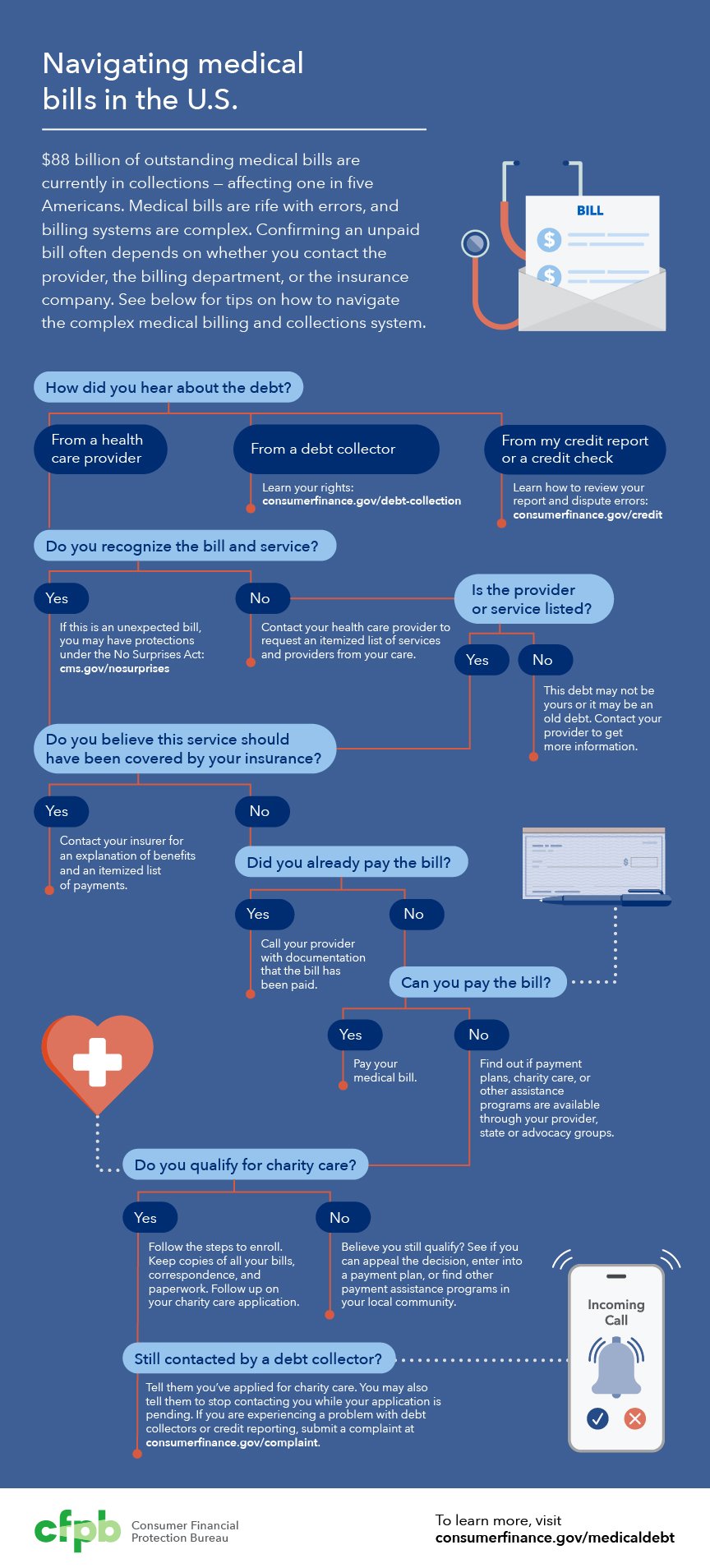

Medical bills are complicated and often hard to understand. Factors like your provider, your health insurance company, and your eligibility for financial assistance or “charity care” will determine whether you owe the bill, and if so, how much. Additionally, laws at the federal and state level may help protect you from some medical bills as well as provide protections from debt collection and credit reporting.

{kind=link}

You can take steps to make sure that the medical bill is correctly calculated and that you get any available financial or necessary legal help. If you do nothing and don’t pay, you could be facing late fees and interest, debt collection, lawsuits, garnishments, and lower credit scores.

Do you owe the bill?

First, make sure that you owe the bill. You could have already paid it. It’s also possible that the provider or debt collector has confused you with someone else with a similar name.

Second, check the charges. If something doesn’t look right, ask for an itemized list of charges. Some questions to consider:

- Are the charges accurate?

- Do they reflect the services you received?

- If you have insurance, do the bills reflect the payment by your insurance and reflect what the provider understood would be covered?

- Do any of the charges indicate a service was “out-of-network” when it wasn’t?

Look for billing errors like being charged for the same service or treatment twice. If you are unsure, talk to the accounting or billing office of your provider. Their number and contact information will be on the billing statement. You want to do this quickly so you can get any charges resolved and to avoid late fees and interest.

Third, if you disagree with the charges or want more information, you have the right to an appeal with your health insurance company . You have a right to both an “internal appeal” and an “external review” of the charges. Check your health insurance policy documents and the “explanation of benefits.”

Finally, remember that you can also dispute a medical bill with a debt collector or a credit reporting company.

Is the bill a “surprise” medical bill?

Effective January 1, 2022, the No Surprises Act (NSA) protects you from “surprise billing” if you have health insurance and provides some protections from surprise medical bills if you are uninsured. If you’re insured, the law bans certain practices, like requiring you to pay out-of-network charges for emergency services. Check and see if it applies to you. This surprise billing usually occurs after you receive care at an out-of-network facility or at an out-of-network provider and your insurance does not cover the out-of-network cost. In these situations, the No Surprises Act can protect you from owing the difference between the out-of-network billed cost and the amount your health insurance paid. Some services, such as ground ambulance transportation services, are NOT protected by the No Surprises Act.

Is there financial help or “charity care” for my medical bills?

Financial assistance programs, sometimes called “charity care,” provide free or discounted health care to people who need help paying their medical bills. The Affordable Care Act (ACA) requires hospitals with 501(c)(3) nonprofit status to have programs to provide this care . Some states have charity care laws that also require additional free or discounted care to be provided by hospitals.

Read more detailed information about financial assistance programs and charity care.

Other protections

Older adults: If you apply for and are covered by the Qualified Medicare Beneficiary (QMB) program, doctors, suppliers, and other providers should not bill you for services and items covered by Medicare, including deductibles, coinsurance, and copayments. If a provider asks you to pay, that’s against the law. If the medical provider won’t stop billing you, call Medicare at 1-800-MEDICARE (1-800-633-4227). TTY users can call (877) 486-2048. If you’re a Qualified Medicare Beneficiary, Medicare can ask your provider to stop billing you and refund any payments you’ve already made.

Veterans: You may qualify for financial hardship assistance . This assistance may include repayment plans, copayment exemption, debt relief, and other assistance. If you need help understanding your bill or dispute the bill, call the VA Health Resource Center at 866-400-1238. Check the VA’s website on financial hardship to learn what options are available in your situation and how to apply for relief. If you have billing disputes you can write a letter explaining the situation and submit it to your local VA medical center with “Billing Dispute” on the envelope .

What if I still owe the bill?

If you still owe the bill or a part of it, here are some options:

- Negotiate the bill down to an amount that you can afford

- Ask if the provider will accept an interest-free repayment plan

- Look for help paying medical bills, prescription drugs, and other expenses. Some nonprofit organizations provide financial help as well as help for drugs necessary for your medical care or even certain medical conditions.

- Be careful about using a credit card or a medical credit card to pay off the bill. There may be high interest and you may lose the ability to negotiate the debt. There may be better options like an interest-free repayment plan.

You also have protections from faulty credit reporting or if you are contacted by a debt collector.

Where can I go if I need more help?

If you are unable to resolve your billing dispute to your satisfaction, you have several options.

Consumer Assistance Programs. Many states provide help for consumers experiencing problems with their health insurance. This state map will help you find assistance in your state or territory.

Centers for Medicare & Medicaid Services offers detailed information about your protections against surprise medical bills.

State agencies such as your state attorney general and state insurance department or insurance commissioner may also offer helpful information as well as a complaint process.

CFPB. If you have a problem with debt collection because of a surprise medical bill, or a problem with credit reporting because of surprise medical charges listed as negative items on your credit report, you can submit a complaint with the CFPB online or by calling (855) 411-CFPB (2372).

Page last modified @