New report shows how young servicemembers build credit histories

Today the Consumer Financial Protection Bureau released a new report exploring the credit records of young servicemembers.

The report shows how credit records co-evolve with military service, from age 18 through age 24. The analysis compares servicemembers who entered the military between 2007 and 2015 based on the age at which they join active duty and based on the time they spend on active duty. It also compares servicemembers’ credit profiles to the credit profiles of civilians.

The report analyzes data from the Bureau’s Consumer Credit Panel (CCP) supplemented with data on military service from the Department of Defense’s Servicemembers Civil Relief Act (SCRA) database. The CCP is a nationally-representative 1-in-48 sample of consumer credit records. Previously, the Bureau released a report on mortgages to first-time homebuying servicemembers using this combined CCP/SCRA dataset.

Young servicemembers often enter the military around the same time they establish a credit record. Their credit profiles may differ from civilians of a similar age because of the types of credit servicemembers need and the types of products they can access. Unlike most civilians, servicemembers may also need to maintain healthy financial profiles in order to maintain a security clearance and stay in the military.

Key findings

Servicemembers and civilians use different credit products

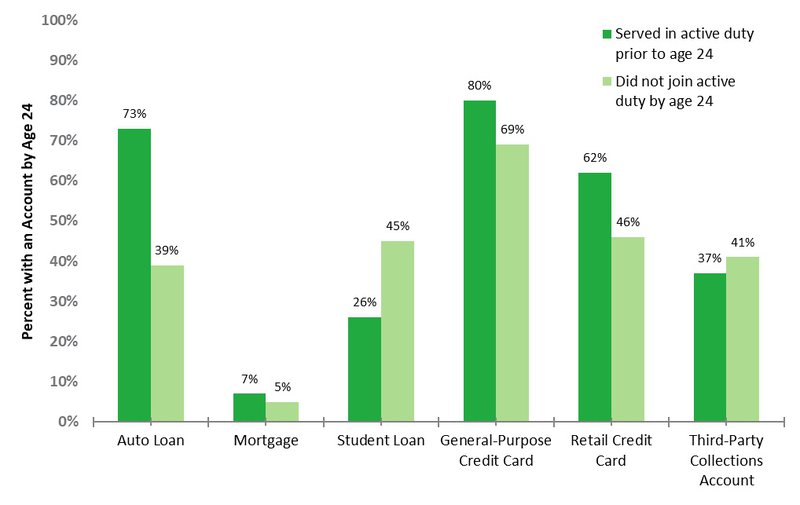

As shown in the figure below, young servicemembers and civilians tended to use different types of credit products. Between ages 18 and 24, servicemembers were more likely than civilians to have had an auto loan or a credit card, and less likely to have had a student loan or debts being collected by a third-party agency, including non-credit debt such as medical or utility bills. Servicemembers were also more likely to have had personal installment loans.

Percentage of consumers with various types of credit accounts between ages 18 and 24

Servicemembers begin opening credit accounts soon after entering the military

Most servicemembers begin active duty service without an auto loan or a credit card, but they begin opening these accounts three to six months after joining the military. Almost 75% of young servicemembers have had an auto loan by age 24, and over 90% have had access to some sort of revolving credit, such as a general-purpose credit card or retail credit card.

Servicemembers who stay in the military longer tend to maintain better credit records

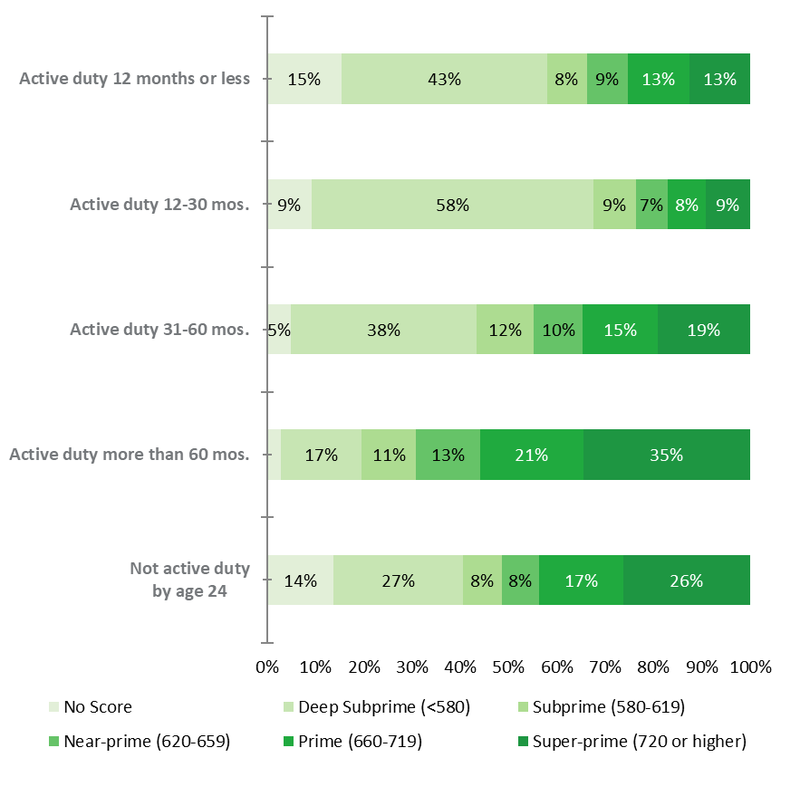

Servicemembers who complete at least three years of service have better credit records by age 24 than servicemembers who leave the military sooner. They have lower rates of delinquency and default, and are also less likely to have non-credit debt in collections, such as a cellphone bill or a utility bill. Servicemembers who serve longer than five years, some of whom have reenlisted and continued in service past their first term of duty, have lower rates of delinquency and better credit scores than civilians who never joined active duty. The graph below shows that 35 percent of these servicemembers maintain super-prime credit scores at age 24, compared to 26 percent of civilians who never joined active duty.

Credit scores at age 24, by amount of time spent in active duty service

Servicemembers’ credit scores decrease after leaving the military

When servicemembers exit, their credit scores decline over the next six to twelve months by an average of more than 20 points. For those who experience a decline, it is often due to a delinquent payment or a default such as an account charge-off, vehicle repossession, or an account being sent to collections. These declines are observed on average for all age groups, no matter the time spent in service, but are most significant for servicemembers who separate with between 12 and 30 months of service. For those servicemembers credit scores decrease by almost 60 points in the year during which they leave the military. This decline leaves 58 percent of these servicemembers with a deep subprime credit score at age 24, as shown in the graph above.

The Bureau and the Department of Defense (DoD) use research like this to guide their financial education and outreach programs. Research can illuminate gaps in financial education, and it can also provide a benchmark to measure the effectiveness of changes to programs over time. For example, pursuant to the 2016 National Defense Authorization Act , DoD began providing financial literacy training at various “touchpoints” throughout a servicemember’s career. When the first cohorts to receive this training start to complete their terms of service, follow-up research could gauge the effectiveness of those changes by comparing how their credit-related behaviors differ from the pre-2016 sample used in this report. This report provides a foundational comparison for future work on servicemembers’ credit behavior.

Dr. James Marrone is an Economist in the Office of Servicemembers Affairs at the Consumer Financial Protection Bureau. Dr. Susan Carter is an Associate Professor of Economics at the United States Military Academy. Mr. Andrew Cohen is the Director for the Office of Financial Readiness in the Office of the Deputy Assistant Secretary of Defense for Force Education and Training.

The views expressed herein are those of the authors and do not reflect the position of the United States Military Academy, the Department of the Army, or the Department of Defense.