Behind on bills: Three steps to help you make tough choices in tight moments

When bills are piling up, it’s important to remember that you’re still in control. While you are ultimately responsible for paying all of your bills on time, there are things you can do if you fall short one month and don’t have enough money to cover everything.

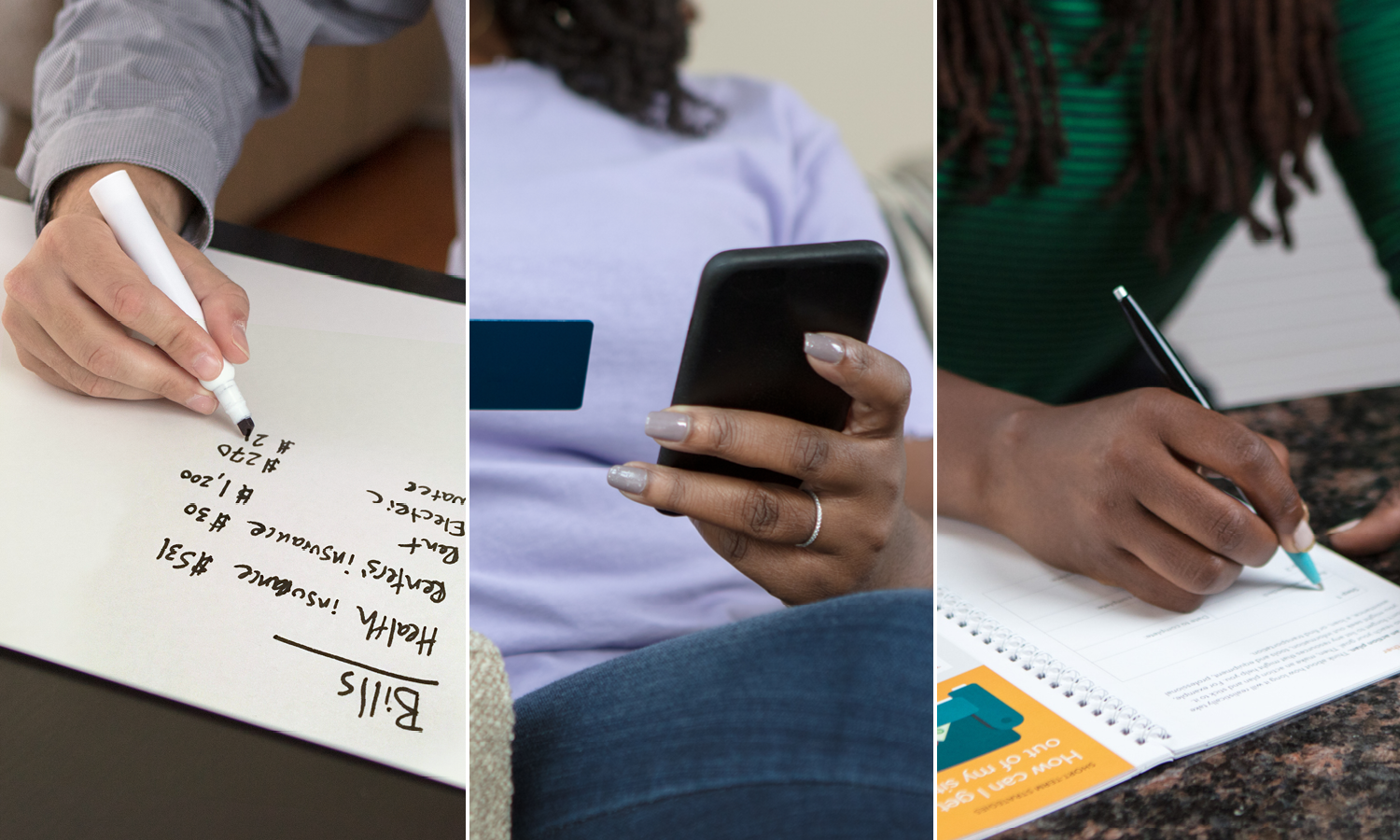

Follow our three easy tips that can help you plan and make the best decisions for your situation.

1. Make a plan

When you’re facing a cash flow emergency, make a list of all of your bills and when they’re due. This step will help you assess your financial obligations.

Consider organizing bills into categories:

- Job or education related expenses, such as transportation to and from work, tools, uniforms, or work-related courses and trainings

- Insurance, such as car insurance, health insurance, or home or renters’ insurance

- Housing related, such as rent, mortgage payments, or utilities

- Other obligations such as credit card bills, loans, medical bills, child support, or childcare

You can also use our bill calendar to help you get a total picture of your monthly bills and identify the weeks you have the most money due.

If you can’t pay all of your bills at once, think about the order you pay them in. Weigh the risks of falling behind on one or more bill. While not ideal, this may prevent you from losing your car or house, having utilities shut off, or getting into serious default on a loan.

2. Call your creditors

If you have to miss a payment, try calling your creditors first to tell them why. Depending on your situation, ignoring your bills could lead to higher interest rates, damage to your credit score, repossession of your car, or foreclosure. Instead, talk to your creditors and explain your situation. They may be willing to forgive a late fee and to make short-term arrangements. For example, if you are in good standing with your creditors, they may be willing to enter into an affordable repayment plan.

If you find you’re often late with a particular bill, negotiate a due date that better lines up with when you get paid or receive income or benefits. Many creditors may be willing to shift the due date if you ask.

3. Track your spending

We also recommend tracking your spending for a short amount of time, like a month. This practice will help you figure out how you’re spending your money and identify where you might be able to adjust your spending to get ahead of upcoming expenses.

According to consumer marketing research, nine out of ten shoppers report that they frequently buy items not on their shopping lists. When people overspend, they may have to dip into savings or borrow money, sometimes at a high cost, to make up for the difference between what they earn and what they spend. Our budget worksheet and spending tracker tool can help you get started.