Data Spotlight: The Impact of Changing Mortgage Interest Rates

Mortgage interest rates have risen over five percentage points since bottoming out in January 2021 at 2.65%, peaking at 7.79% in October 2023. Since then, rates have eased to around 6.2% in September 2024. These higher rates are significantly decreasing housing affordability, with the mortgage payment on a $400,000 loan rising over $1,200 from trough to peak. Home prices have also continued to rise, adding to affordability pressure. However, as interest rates decrease, millions of borrowers may be able to refinance their mortgages and achieve more affordable payments. This analysis examines the impact of higher interest rates on home affordability, the distribution of interest rates on existing mortgages, and the potential for refinancing as interest rates decrease.

Post-pandemic interest rate trends

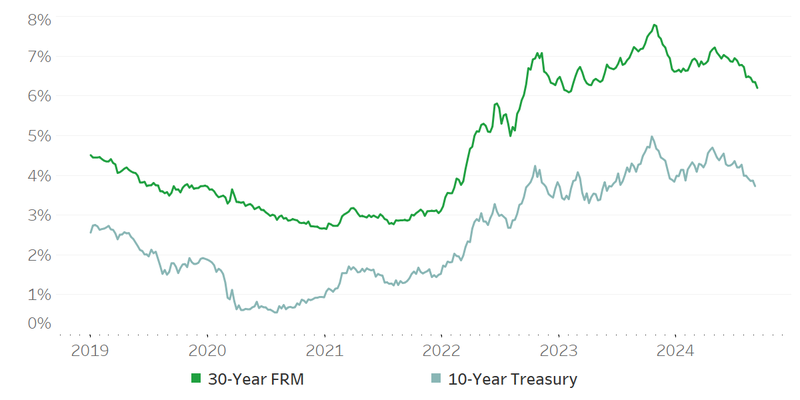

During the COVID-19 pandemic, mortgage interest rates dropped to historically low levels, reaching 2.65% in January 2021. That low-rate environment was marked by substantial refinancing activity; researchers at the Federal Reserve Bank of Boston estimate that individuals who refinanced from January 2020 to October 2020 saved $5.3 billion annually . When mortgage interest rates rose to 5% in April 2022, it was the first time interest rates had been that high since 2011—more than eleven years earlier.

Much of the rise in interest rates is directly related to global monetary policy responses to post-pandemic inflation. However, additional pressure has been placed on mortgage rates through a combination of effects from the Federal Reserve’s retreat from purchasing mortgage-backed securities (MBSs) and changes in the expected prepayment speeds of newly originated MBSs that combined has led to an increased spread between 10-year Treasuries and mortgage securities. This spread has been around 250 bps, which is roughly 50 bps lower than last year, but still higher than pre-pandemic levels of around 2.00% or during the low-interest rate environment of 2020-2021, where it bottomed out around 1.25%. Mortgage interest rates have already started to decline in anticipation of the Federal Reserve lowering the federal funds rate, and further actions by the Federal Reserve will continue to affect the trajectory of the mortgage rates.

Figure 1: Mortgage interest rates and Treasury rates

Source: Freddie Mac Primary Mortgage Market Survey and Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity

Effects of elevated interest rates on affordability

Higher interest rates combined with higher home prices have contributed to a lack of mortgage affordability. As shown in the table below, this large increase in rates alone produces a significant strain on housing affordability adding $1,265 to principal and interest payments on a $400,000 loan (a 78% increase, from $1,612 to $2,877) from trough to peak. Even at the slightly lower rates in today’s market that increase has added $838, or 52%. In addition to the impact from rate increases, the surge in home prices over the same period has exacerbated the increase in payments, as further shown in the table below. Looking at both factors the payment on a median priced home with a 5% down payment increased $1,532 or 113% from 2021 to 2023. That increase remained at $1,040 or 77% even with the slight pull back in both interest rates and home prices.

Figure 2: Example mortgage payments

| Date | Interest rate | P&I payment on $400,000 loan | Median sales price | P&I on median home sold with 5% down payment |

|---|---|---|---|---|

1/7/2021 |

2.65% |

$1,612 |

$355,000 |

$1,359 |

10/26/2023 |

7.79% |

$2,877 |

$423,200 |

$2,891 |

9/12/2024 |

6.20% |

$2,450 |

$412,300 |

$2,399 |

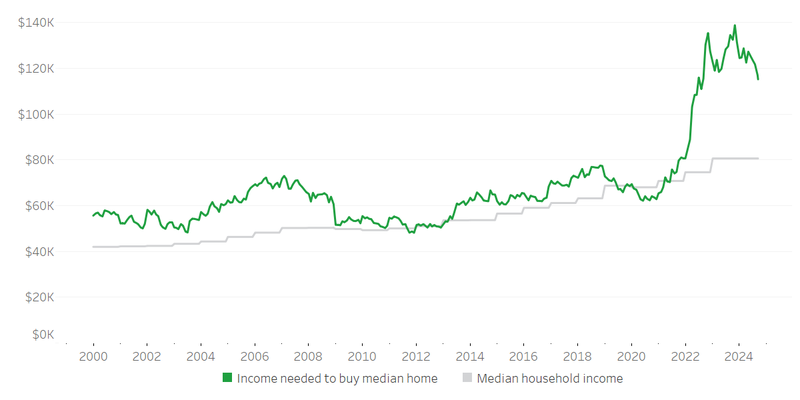

The combination of higher rates and higher home prices has drastically changed housing affordability for the typical household.1 In 2019, the typical household earning $69,000 a year could buy the median home on the market and expect to spend about 26% of their monthly income on the principal and interest (P&I) payments for their mortgage. During the early years of the Covid-19 pandemic, interest rates fell to historic lows and millions of consumers purchased homes or refinanced to lower interest rates. Home prices were rising faster than incomes, but the low interest rates made mortgage payments more affordable, at least on a national level. A homebuyer who got a mortgage in January 2021, when interest rates were at their all-time low of 2.65%, would have paid about $1,359 in principal and interest monthly, or about 23% of the median household income.

Figure 3: Income needed to buy the median home

Note: Calculations assume the borrower has a 5% down payment and are based on median household income, median sales price, and interest rates on 30-year fixed rate mortgages.

Source: U.S. Census Bureau, Median Household Income in the United States; U.S. Census Bureau and U.S. Department of Housing and Urban Development, Median Sales Price of Houses Sold for the United States; and Freddie Mac Primary Mortgage Market Survey

Interest rates rose rapidly in 2021, rising four percentage points in less than a year. As rates rose, homeownership became less affordable for many Americans. Higher interest rates also meant fewer homes were available for sale because homeowners who had locked in low-rate mortgages were hesitant to move, creating a “lock in effect.” By the time rates peaked in October 2023 at 7.79%, the principal and interest payment for the median priced home had jumped 78% to $2,891.

Interest rates have declined from their peak, offering some respite to potential homeowners, but housing affordability is still a challenge. Today, the typical household would have to spend about 36% of their monthly income to afford the monthly mortgage payment for the median home. If they decided instead to stick to a budget of 25%, they would need to increase their income by 59% to $119,000, or interest rates would need to fall to 2.5%, or home prices would need to fall by 37%.

Potential for Future Refinances

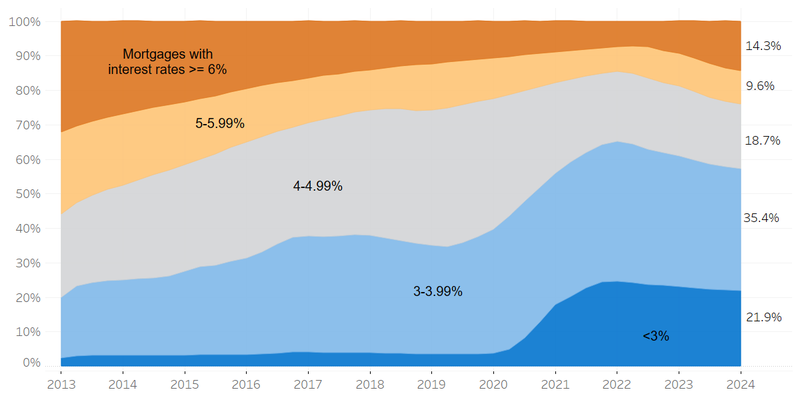

As a result of the trends described above, the mortgage market is characterized by two very different groups. Nearly 60% of the 50.8 million active mortgages have interest rates below 4%, and many of those homeowners may feel locked into their current home and loan. But more than a fifth of all mortgages have interest rates at or above 5%, with 14.3% of mortgages at or above 6%. Approximately 60% of those loans were originated in the last two years. Figure 4 below shows how these interest rate cohorts have changed over time.

As interest rates fall, millions of borrowers may be able to refinance and get more affordable payments. As interest rates eased down to 6.5%, about 2.5 million borrowers could already refinance and save at least 75 basis points (0.75%) on their interest rate, according to data from ICE Mortgage Technology. A reduction in rate from 7.25% to 6.5% would result in a $200 monthly savings on a $400,000 loan with a similar term. If interest rates fall to 5.5%, more than 7 million borrowers can potentially refinance, and over 5 million of these refi candidates got their mortgages in the past three years.

Figure 4: Interest rates on existing mortgages

Note: Interest rates are the contract interest rate at origination.

Source: National Mortgage Database

However, past refinancing booms suggest that eligible borrowers may not get the opportunity to refinance. Even as interest rates fell to historic lows in 2020 and 2021, about 3.7 million mortgages (7.4%) still had interest rates of at least 6% and another 3.5 million (7%) had interest rates of at least 5%. Researchers at the Atlanta Fed found that Black and Hispanic borrowers were less likely to refinance than other borrowers, even after controlling for factors like credit scores, home equity, and income. According to researchers from the FDIC , when lenders are capacity constrained, they target borrowers with high loan balances, high incomes, and high credit scores. These past experiences show that when interest rates fall and refinancing becomes more attractive, some consumers will still be left behind.

For millions of borrowers, the opportunity to refinance would create significant savings and potentially improve financial stability. Additionally, refinancing frees up homeowners’ finances to engage in other types of spending, which can benefit the economy. The CFPB will continue to monitor and report on refinancing activity and industry practices that encourage or discourage borrowers seeking to refinance. The CFPB is also exploring ways to streamline the refinancing process and reduce closing costs.

Endnotes

-

We are defining a “typical household” as one with the national median household income.

↩

Page last modified @