CFPB Aims to Simplify Mortgage Closing Documents

Agency Soliciting Public Feedback as Part of the ‘Know Before You Owe’ Mortgage Project

WASHINGTON − Today, the Consumer Financial Protection Bureau (CFPB) announced the second phase of its Know Before You Owe mortgage project, which will combine the two forms consumers get before finalizing a home loan into a single, easy-to-understand mortgage closing document. The CFPB is asking for public feedback on two alternative prototypes, which are designed to clearly explain the final details of the loan and closing costs.

The mortgage closing document prototypes can be found at: www.consumerfinance.gov/knowbeforeyouowe

“Purchasing a home is one of the biggest financial decisions a consumer can make,” said Raj Date, Special Advisor to the Secretary of the Treasury on the CFPB. “The second phase of our Know Before You Owe mortgage project is aimed at simplifying the federal disclosures consumers have to tackle at the closing table. Our goal is to help make the costs and risks clear at all stages of the mortgage process – from shopping for a mortgage to signing on the dotted line.”

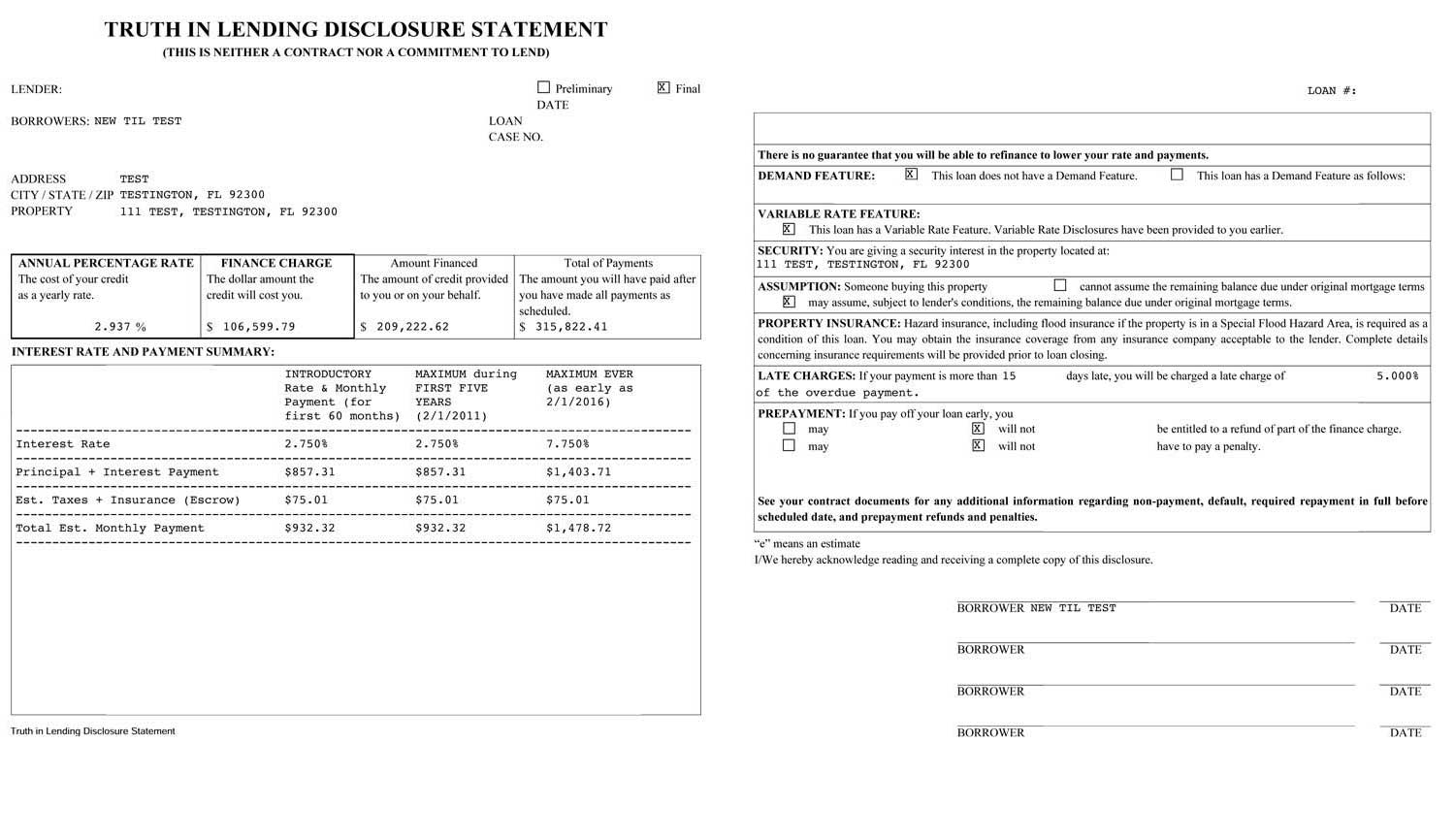

Current federal law says that at or before closing on a mortgage loan, borrowers generally must be given two documents – the federal Truth in Lending Disclosure and the HUD-1 Settlement Statement. The CFPB is now combining these two forms. The CFPB is also consolidating other new and current federal mortgage disclosure requirements – boiling down unnecessary paperwork by as much as 50 percent.

{kind=link}

The mortgage closing document prototypes build upon the feedback received in the first phase of the Know Before You Owe mortgage project, which focused on the loan estimates consumers receive shortly after they apply for a mortgage. Over five rounds of testing different prototypes of these estimates, the CFPB received feedback from more than 24,000 members of the public, industry participants, and market experts. The second phase of this project incorporates that feedback into prototypes that provide more detailed information to consumers about their final loan terms and costs.

With CFPB’s prototype mortgage closing documents, consumers can clearly see whether the final loan terms and costs match the terms and costs quoted in the estimate provided after application. They can determine whether the interest rate or monthly payments could change after closing. And they can clearly see projected payments over the life of the loan. The goal with the new form is to provide information in a clear and simple way that consumers will find easier to use and understand and that industry will find less burdensome.

In addition to soliciting public feedback online, CFPB is conducting qualitative testing on the prototypes in cities across the country starting today in Des Moines, Iowa. This testing will entail one-on-one conversations with consumers, lenders, brokers, and other industry professionals. The Bureau expects to conduct four rounds of testing and revisions through February 2012. The CFPB also plans to issue draft forms for public comment as part of notice and comment rulemaking procedures in July 2012.

The CFPB was created by the Dodd-Frank Wall Street Reform and Consumer Protection Act. Consistent with its congressional mandate in the Dodd-Frank Act, the CFPB is consolidating certain federally required mortgage forms – the Truth in Lending disclosure, the Good Faith Estimate, and the HUD-1 Settlement Statement. These forms are required by the Truth in Lending Act and the Real Estate Settlement Procedures Act, responsibility for which transferred from other federal agencies to the CFPB when the agency officially launched on July 21, 2011.