Understand your prepaid card disclosure

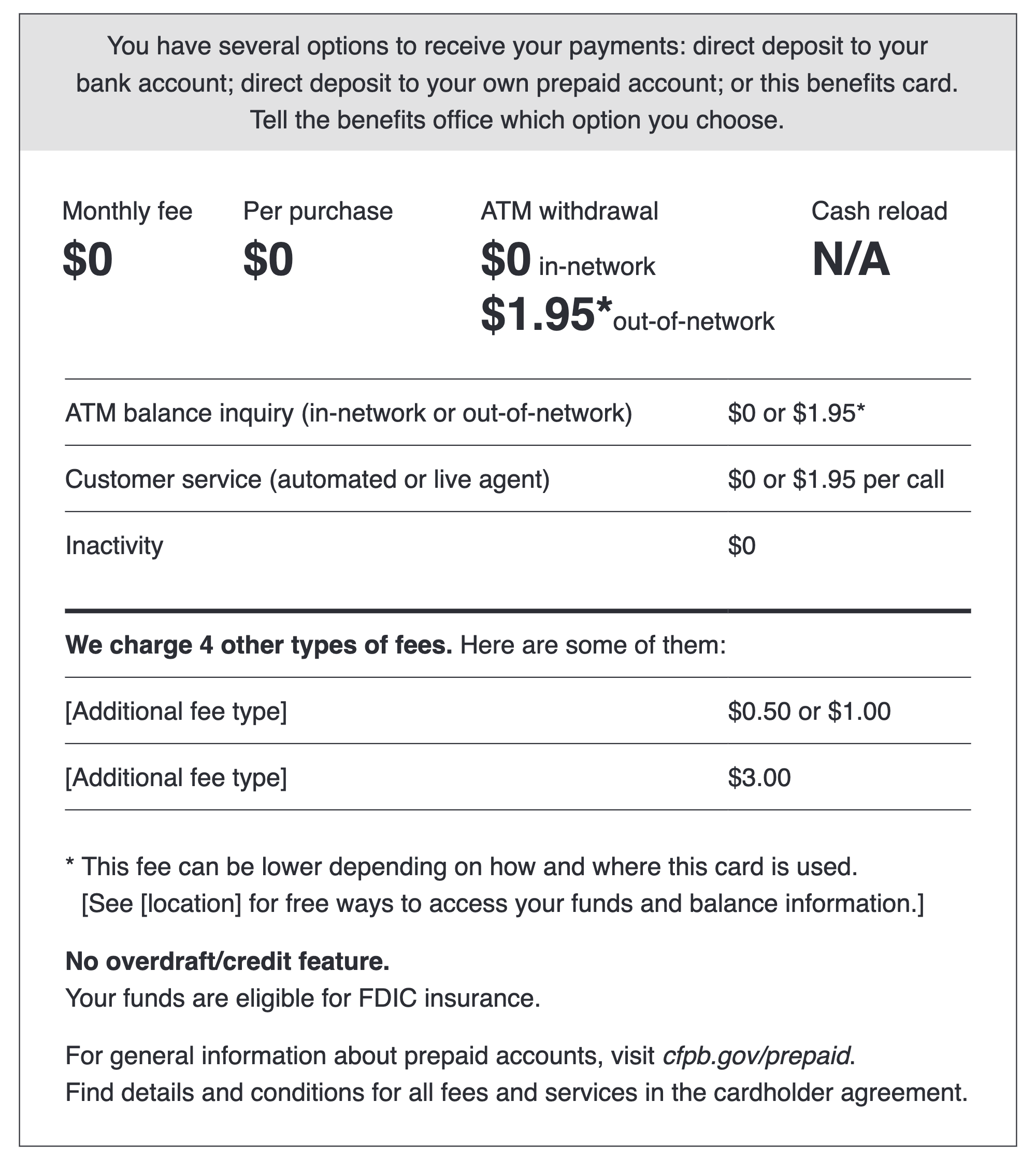

A prepaid card provider has to disclose fees before you buy the card. The sample form below shows the highest amount that can be charged. It also shows how certain fees may be lower depending on how or where you use the card.

Sample prepaid card disclosure

How to get information about all fees

If you get your card in a store, a short summary of key fees and information will be on the outside of or visible through the prepaid card packaging. This short form will include a toll-free number and a website to view all the fees that may be charged on the prepaid card and other important information.

If you get your card in other settings, like online or over the phone, the card provider needs to give you this form on paper or electronically. This form will tell you where to find all fees and services (usually in the cardholder agreement).

Register your card as soon as possible

It is important to register your prepaid card as soon as possible. Your prepaid card provider is not required to protect you from loss, theft, or fraud on your card account until you successfully register it. If you apply for a card online, you will usually register it before you get the prepaid card. But if you buy a card in a store, be sure to register it to get full protection in case your card is lost or stolen.

Page last modified @