Consumer Financial Protection Circular 2022-07

Reasonable investigation of consumer reporting disputes

Questions presented

- Are consumer reporting agencies and the entities that furnish information to them (furnishers) permitted under the Fair Credit Reporting Act (FCRA) to impose obstacles that deter submission of disputes?

- Do consumer reporting agencies need to forward to furnishers consumer-provided documents attached to a dispute?

Responses

- No. Consumer reporting agencies and furnishers are liable under the FCRA if they fail to investigate any dispute that meets the statutory and regulatory requirements, as described in more detail below. Enforcers may bring claims if consumer reporting agencies and furnishers limit consumers’ dispute rights by requiring any specific format or requiring any specific attachment such as a copy of a police report or consumer report beyond what the statute and regulations permit.

- It depends. Enforcers may bring a claim if a consumer reporting agency fails to promptly provide to the furnisher “all relevant information” regarding the dispute that the consumer reporting agency receives from the consumer. While there is not an affirmative requirement to specifically provide original copies of documentation submitted by consumers, it would be difficult for a consumer reporting agency to prove they provided all relevant information if they fail to forward even an electronic image of documents that constitute a primary source of evidence.1

Background

Information contained in consumer reports has critical effects on Americans’ daily lives. Consumer reports are used to evaluate consumers’ eligibility for loans and the interest rates they pay, their eligibility for insurance and the premiums they pay, their eligibility for rental housing, and their eligibility for checking accounts. Prospective employers commonly use consumer reports in their hiring decisions.2 Given the importance of this information, Congress enacted the FCRA to “prevent consumers from being unjustly damaged because of inaccurate or arbitrary information in a credit report.”3

A central component of the protections against inaccurate information is the requirement to conduct a reasonable investigation of consumer disputes. Since its enactment, the FCRA has required consumer reporting agencies to investigate consumer disputes.4 To further ensure that consumer reports are accurate, in 1996 Congress amended the FCRA to also impose “duties on the sources that provide credit information to CRAs [consumer reporting agencies], called ‘furnishers’ in the statute.”5 Thus, when consumer reporting agencies and furnishers are properly notified of a dispute about information furnished in a consumer report, both consumer reporting agencies and furnishers must conduct a reasonable investigation of the dispute.6

These responsibilities are part of the FCRA’s overall framework for ensuring accuracy in consumer reports. Consumers are in a good position to identify inaccurate information in their consumer reports, and timely and responsive investigations of these identified inaccuracies is crucial to the FCRA’s purpose of ensuring fair and accurate consumer reporting.

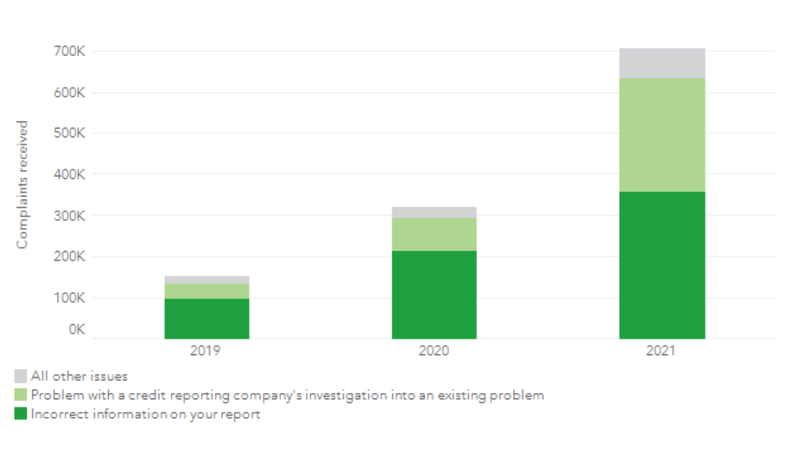

Despite Congress’s repeated efforts to promote accuracy by requiring reasonable investigation of disputes, consumers continue to report problems with accuracy and dispute investigations. Between January and September 2021, the CFPB received more than 500,000 complaints about credit or consumer reporting; the most common issue they identified was incorrect information on a credit report.7 In each of the past three calendar years, the top two most frequently identified issues in complaints submitted to the CFPB were “Incorrect information on your report” and “Problem with a credit reporting company’s investigation into an existing problem.”

Figure 1: Credit or Consumer Reporting Complaints to the CFPB 2019 - 2021

The CFPB is responsible for issuing rules and enforcing compliance with these provisions of the FCRA.8 The FCRA can also be enforced by other federal government agencies and states,9 and through private actions brought by consumers.10 The CFPB is issuing this Circular to emphasize that certain practices involving the failure to conduct a reasonable investigation of disputes can violate the FCRA.

Analysis

Consumer reporting agencies and furnishers cannot avoid the obligation to conduct a reasonable investigation of disputes by making consumers satisfy demands other than those specified by statute or regulation.

The CFPB is aware that consumer reporting agencies and furnishers have sought to evade the obligation to investigate disputes by requiring consumers to submit particular items of information or documentation with a dispute before the entity will conduct its investigation of the dispute. Examples of this conduct include:

- Consumer reporting agencies that require a consumer to provide a recent copy of the consumer’s report or file disclosure before investigating disputes despite the consumer providing sufficient information to investigate the disputed information;11

- Furnishers that require a consumer to provide additional specific documents even though the consumer has already provided the supporting documentation or other information reasonably required to substantiate the basis of a direct dispute;12 and

- Consumer reporting agencies or furnishers that require a consumer to attach a completed proprietary form before investigating the consumer’s dispute.13

Enforcers may consider bringing an action under the FCRA when furnishers and consumer reporting agencies require consumers to provide documentation or proof documents, other than as described in the statute or regulation, as a precondition to investigation. For disputes received directly from a consumer, a consumer reporting agency or furnisher must reasonably investigate the dispute unless they have reasonably determined that the dispute is frivolous or irrelevant.14 If such a determination is made, the consumer reporting agency or furnisher must notify the consumer of such determination within five business days of the determination and identify the additional information needed from the consumer to investigate the dispute.15 Further, furnishers are not permitted to deem disputes as frivolous or irrelevant if the dispute has been provided to the furnisher from a consumer reporting agency pursuant to FCRA Section 623(b).16

Accordingly, consumer reporting agencies and furnishers must reasonably investigate disputes received directly from consumers that are not frivolous or irrelevant – and furnishers must reasonably investigate all indirect disputes received from consumer reporting agencies – even if such disputes do not include the entity’s preferred format, preferred intake forms, or preferred documentation or forms.

Consumer reporting agencies must provide to the furnisher all relevant information regarding the dispute that it received from the consumer.

Enforcers may bring a claim if a consumer reporting agency fails to promptly provide to the furnisher “all relevant information” regarding the dispute that the consumer reporting agency receives from the consumer.17 Through its supervision, the CFPB has found that consumer reporting agencies tend to ingest dispute information from consumers using automated protocols, and they also share dispute information with furnishers electronically.18 The use of these technologies has reduced the cost and time to transmit relevant information.

When transmitting information about a dispute, a consumer reporting agency may be able to demonstrate that it has transmitted “all relevant information” even if it does not provide original documents in paper form. However, given that primary sources of evidence provided by consumers can be dispositive in determining whether there has been a furnishing error, and given that the character of a primary source of evidence is probative and thus relevant to the investigation,19 it will be difficult for a consumer reporting agency to prove that it complied with the FCRA if it does not provide electronic images of primary evidence for evaluation by the furnisher.20

The consumer reporting agency’s failure to provide the furnisher with all relevant information limits the furnisher’s ability to reasonably investigate the dispute. A furnisher must “review all relevant information” provided by the consumer reporting agency.21 Accordingly, consumer reporting agency compliance with the obligation to provide all relevant information is crucial to the consumer’s right to have their dispute reasonably investigated.

Endnotes

- Examples of primary sources of evidence include but are not limited to documents submitted by a consumer in support of a dispute such as copies of letters from creditors, bank statements, checks, or periodic billing statements.

- See, generally Consumer Financial Protection Bureau, Key Dimensions and Processes in the U.S. Credit Reporting System (2012), https://files.consumerfinance.gov/f/201212_cfpb_credit-reporting-white-paper.pdf .

- S. Rep. No. 91-517, at 1 (1969).

- 84 Stat. 1114, 1132 (Oct. 26, 1970).

- Gorman v. Wolpoff & Abramson, LLP, 584 F.3d 1147, 1153 (9th Cir. 2009).

- See, e.g., 15 U.S.C. 1681i(a)(1)(A) (Consumer reporting agency obligation to “conduct a reasonable reinvestigation to determine whether the disputed information is inaccurate”); 15 U.S.C. 1681s-2(b)(1) (furnisher obligation to “conduct an investigation with respect to the disputed information” for disputes provided b y a consumer reporting agency); 12 CFR 1022.43(e)(1) (furnisher obligation to “conduct a reasonable investigation with respect to the disputed information” for disputes sent directly from a consumer); see also Johnson v. MBNA America Bank, NA, 357 F.3d 426, 431 (4th Cir. 2004)(holding that furnishers receiving indirect disputes from consumer reporting agencies must “conduct a reasonable investigation of their records to determine whether the disputed information can be verified.”).

- See Consumer Financial Protection Bureau, Annual Report of Credit and Consumer Reporting Complaints (Jan. 2022), at 21, 30, https://files.consumerfinance.gov/f/documents/cfpb_fcra-611-e_report_2022-01.pdf .

- See, e.g., 12 U.S.C. 5481(12)(F), 5512(b), 5514(c), 5515(c), and also Sub title E (12 U.S.C.5561 –5567); 15 U.S.C. 1681s(b)(1)(H), (e). Authority over 15 U.S.C. 1681m(e) and 1681w are limited to the Federal banking agencies, the NCUA, the FTC, the CFTC, and SEC.

- 15 U.S.C. 1681s. States can directly bring actions under FCRA. See 12 U.S.C. 1681s(c).States can al so bring actions under the Consumer Financial Protection Act (CFPA) against “covered persons” and “service providers” based upon violations of federal consumer financial laws, including the FCRA. See Authority of States to Enforce the Consumer Financial Protection Act of 2010, 87 FR 31940 (May 26, 2022).

- 15 U.S.C. 1681n, 1681o.

- See, e.g., Consumer Financial Protection Bureau, Supervisory Highlights(Spring 2014), at 10, https://files.consumerfinance.gov/f/201405_cfpb_supervisory-highlights-spring-2014.pdf .

- See, e.g., Complaint at 15, CFPB v. Fair Collections & Outsourcing, Inc., D. Md. No. 19-Civ-2817 (Filed Sep. 25, 2019).

- With respect to furnisher direct disputes, see 74 FR 31,484, 31,500 (July 1, 2009) (“Some industry commenters also suggested that the Agencies issue a model direct dispute complaint form, with some advocating that consumers be required to use the model complaint form. The Agencies decline to adopt these suggestions because such requirements would cause otherwise valid disputes to b e rejected as frivolous or irrelevant due solely to the consumer's failure to meet a technical requirement that probably would be unknown to the consumer.”)

- 15 U.S.C. 1681i(a)(3)(A) (identifying which disputes the consumer reporting agency can determine to be frivolous or irrelevant); 12 CFR 1022.43(f)(1) (identifying which disputes the furnisher can determine to be frivolous or irrelevant).

- 15 U.S.C. 1681i(a)(3) (Consumer reporting agency frivolous or irrelevant determination); 12 CFR 1022.43(f) (furnisher direct dispute frivolous or irrelevant determination).

- 15 U.S.C. 1681s-2(b). See Brief for Consumer Financial Protection Bureau and Federal Trade Commission as Amici Curiae Supporting Plaintiff-Appellant, Ingram v. Waypoint Resource Group, LLC, Third Circuit Court of Appeals (No. 21-2430).

- 15 U.S.C. 1681i(a)(2)(A).

- Consumer Financial Protection Bureau, Bulletin 2013-09 (Sep. 4, 2013), at 1, https://files.consumerfinance.gov/f/201309_cfpb_bulletin_furnishers.pdf (alerting furnishers to the fact that consumer reporting agencies have begun forwarding images of relevant documentation to furnishers as part of the reasonable investigation of disputes).

- For example, a copy of a bill supporting the consumer’s dispute conveys information regarding the persuasiveness of a consumer’s dispute that data about the bill would not.

- Federal Trade Commission, 40 Years of Experience with the Fair Credit Reporting Act: An FTC Staff Report with Summary of Interpretations (Jul. 2011), at 77, https://www.ftc.gov/sites/default/files/documents/reports/40-years-experience-fair-credit-reporting-act-ftc-staff-report-summary-interpretations/110720fcrareport.pdf (“ACRA does not comply with this provision if it merely indicates the nature of the dispute, without communicating to the furnisher the specific relevant information received from the consumer. For example, if the consumer claimed “never late” and submitted documentation (such as cancelled checks) to support his/her dispute, a CRA does not comply with the requirement that is provide “all relevant information” if it simply notifies the furnisher that the consumer disputes the payment history without communicating the evidence received.”).

- 2115 U.S.C. 1681s-2(b)(1)(B).

Page last modified @