Examining the factors driving high credit card interest rates

When consumers face unexpected expenses and lack the cash to make it from one paycheck to the next, credit cards can provide essential flexibility. More than 175 million Americans have at least one credit card, and at any given time, about half of active credit card accounts carry a balance

In the coming months, even more people may turn to their credit cards, as increasing prices for necessities like groceries and gas upend their budgets. But this borrowing comes at a cost. With today’s interest rates, a person with a $5,000 credit card balance could pay an additional $1,000 in interest over the course of a year. Consumer reliance on credit cards as a source of borrowing justifies a closer look at what’s driving interest rates, as credit card market profitability increases.

Examining the factors influencing credit card interest rates

Reforms in the Credit Card Accountability Responsibility and Disclosure Act of 2009 (“CARD Act”) advanced competition and saved consumers billions of dollars by restricting harmful back-end or hidden pricing practices

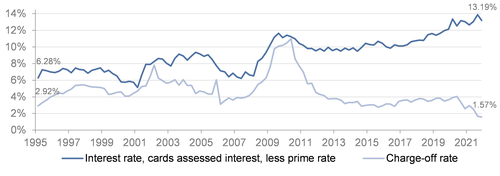

Charge-offs

In 2021, the risk margin on credit cards reached all-time highs even though actual delinquencies and defaults fell to record lows (Figure 1). The margin is the difference between the prime rate, the benchmark most commercial banks use to set cardholders’ annual percentage rate (APR), and the average APR on credit cards assessed interest

Before the Great Recession, the charge-off rate – a measure of accounts considered uncollectable after extreme delinquency – and issuers’ margin moved in tandem. But then, as the economy recovered, credit card companies did not decrease their prices accordingly, despite seemingly lower risk of default.

During the COVID-19 pandemic, issuers’ margins and charge-off rates diverged even further.

Figure 1: Risk Margin; Charge-Off Rate (Federal Reserve)

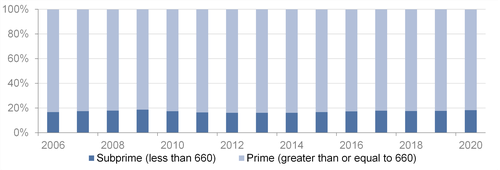

Subprime accounts

Previously, an increase in new credit card accounts for people with lower credit scores generally led to a rise in average credit card interest rates, as people with subprime scores – less than 660 – are typically offered a higher rate due to a greater risk of default. Yet, since 2015, the share of credit card holders with subprime scores has remained stable, representing less than one-fifth of total accounts (Figure 2). Therefore, high rates persist even though presumably riskier subprime loans have not increased.

Figure 2: Share of Total Accounts by Credit Score Tier (CCP)

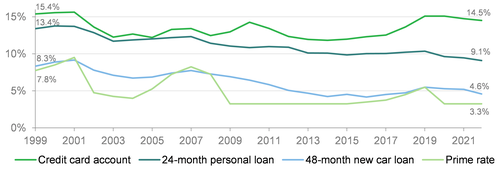

Prime rate

Compared to other lending products, credit card pricing appears to be less responsive to macroeconomic trends like changes in the cost of funds – a measure of how much banks spend to acquire money to lend to consumers – as represented by the prime rate (Figure 3). Since 1995, the prime rate has fallen from a high of nine percent to a low of three percent

Figure 3: Commercial Bank Interest Rates (Federal Reserve

Credit card profitability

The apparent mismatch between credit card interest rates and the risk and cost of lending may explain part of the markets’ outsized profits. In 2021, large credit card banks reported an annualized return on assets of near seven percent

Since 2005, the same top six credit card issuers have accounted for over two-thirds of total balances. As the credit card market continues to be dominated by a few key players, the CFPB plans to evaluate whether trends, like increasing rewards and high switching costs, explain the industry’s persistently high interest rates or if anti-competitive practices, such as those that prevent consumers from receiving better offers, have driven issuers’ profits at cardholders’ expense.

The views expressed here are those of the authors and do not necessarily reflect the views of the Consumer Financial Protection Bureau. Links or citations in this post do not constitute an endorsement by the Bureau.