Appendix H to Part 1022 - Model Forms for Risk-Based Pricing and Credit Score Disclosure Exception Notices

1. This appendix contains four model forms for risk-based pricing notices and three model forms for use in connection with the credit score disclosure exceptions. Each of the model forms is designated for use in a particular set of circumstances as indicated by the title of that model form.

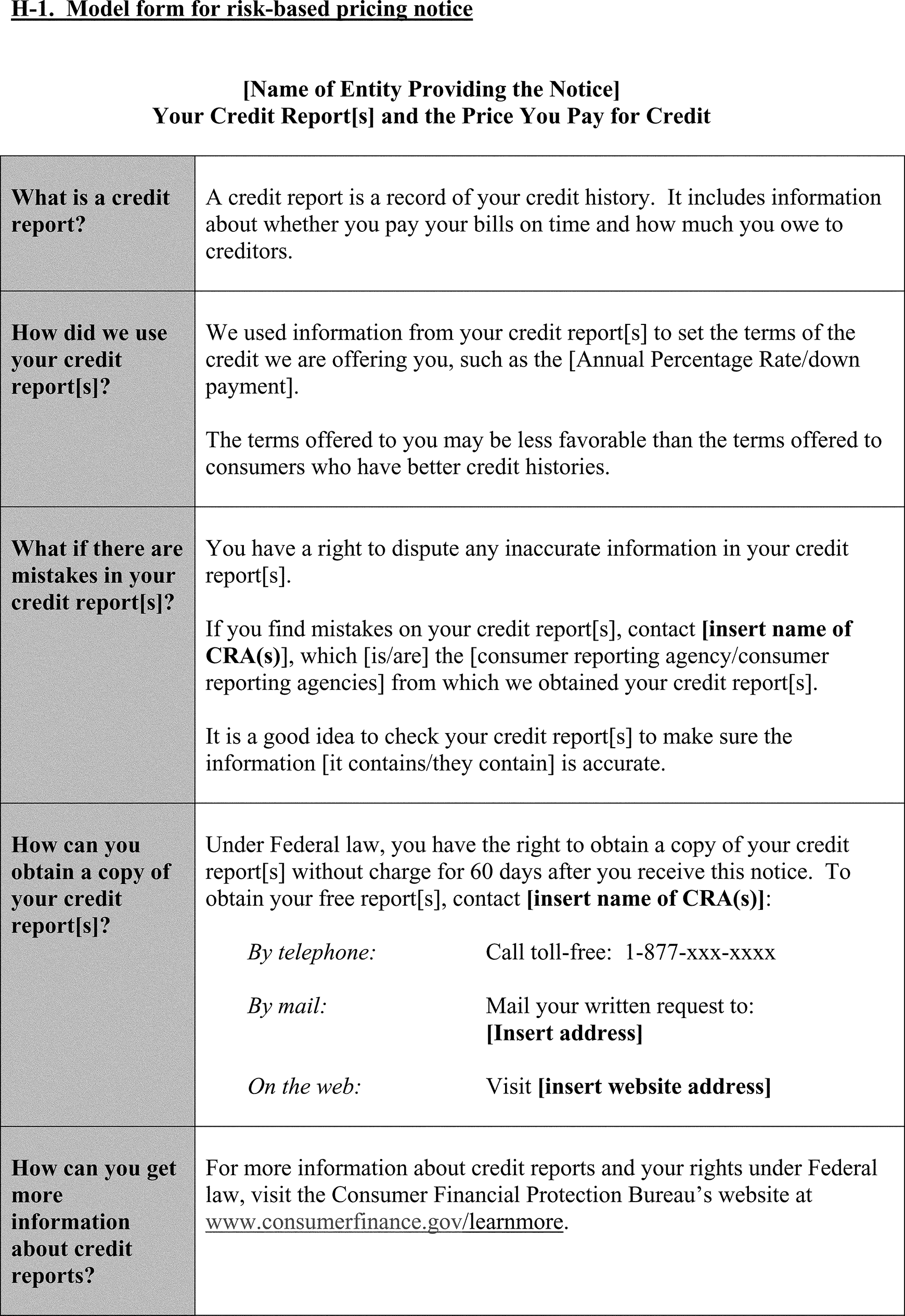

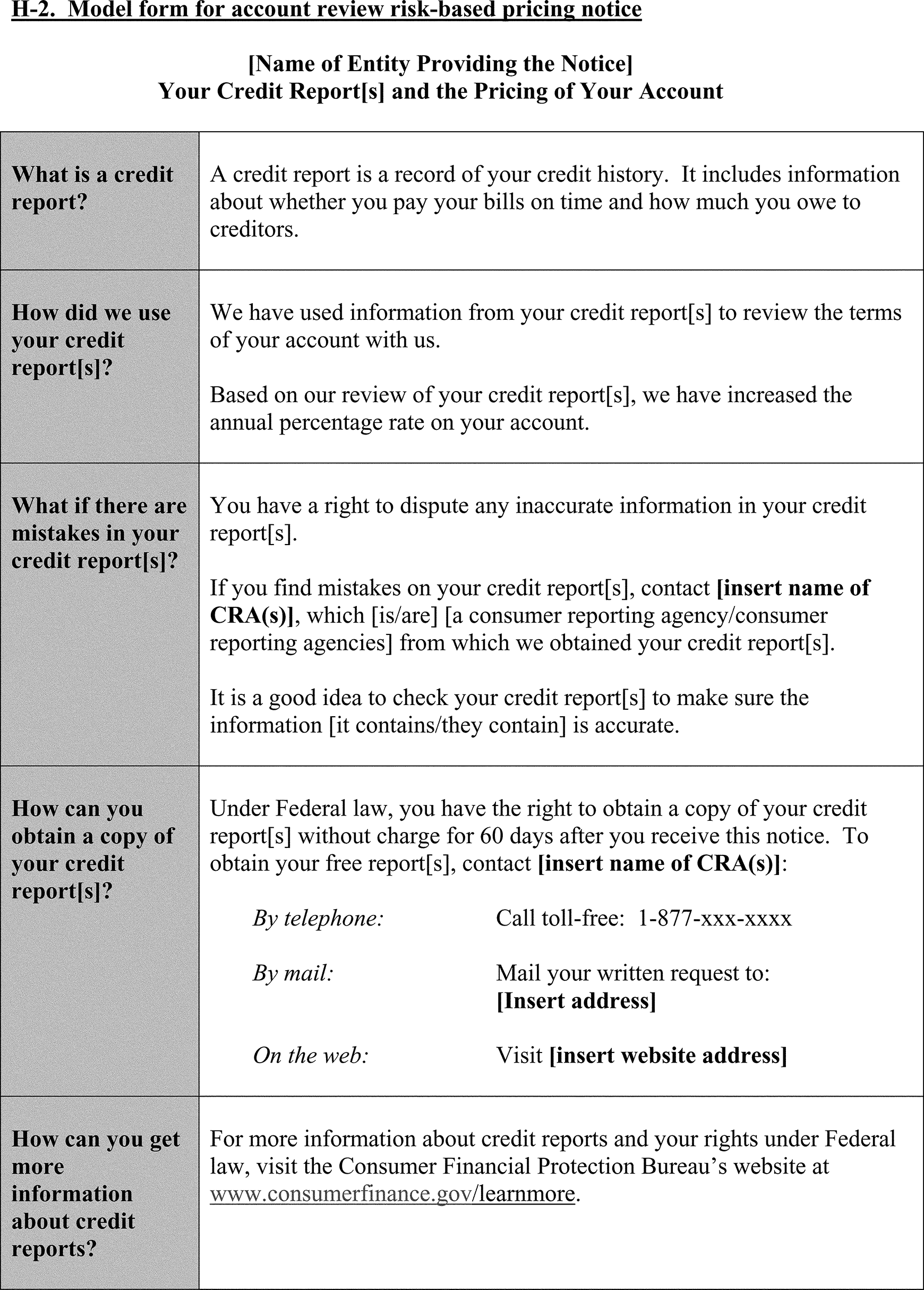

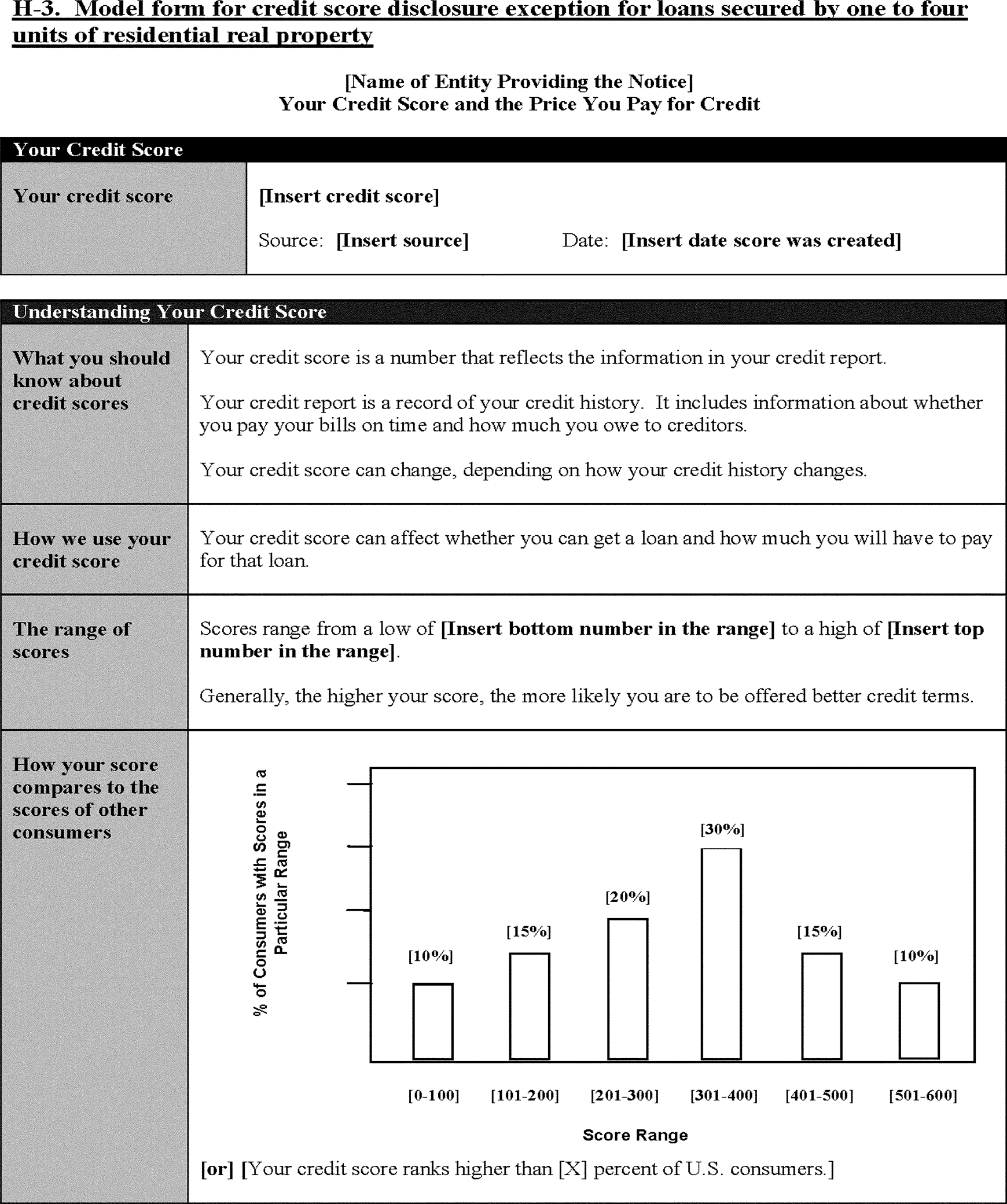

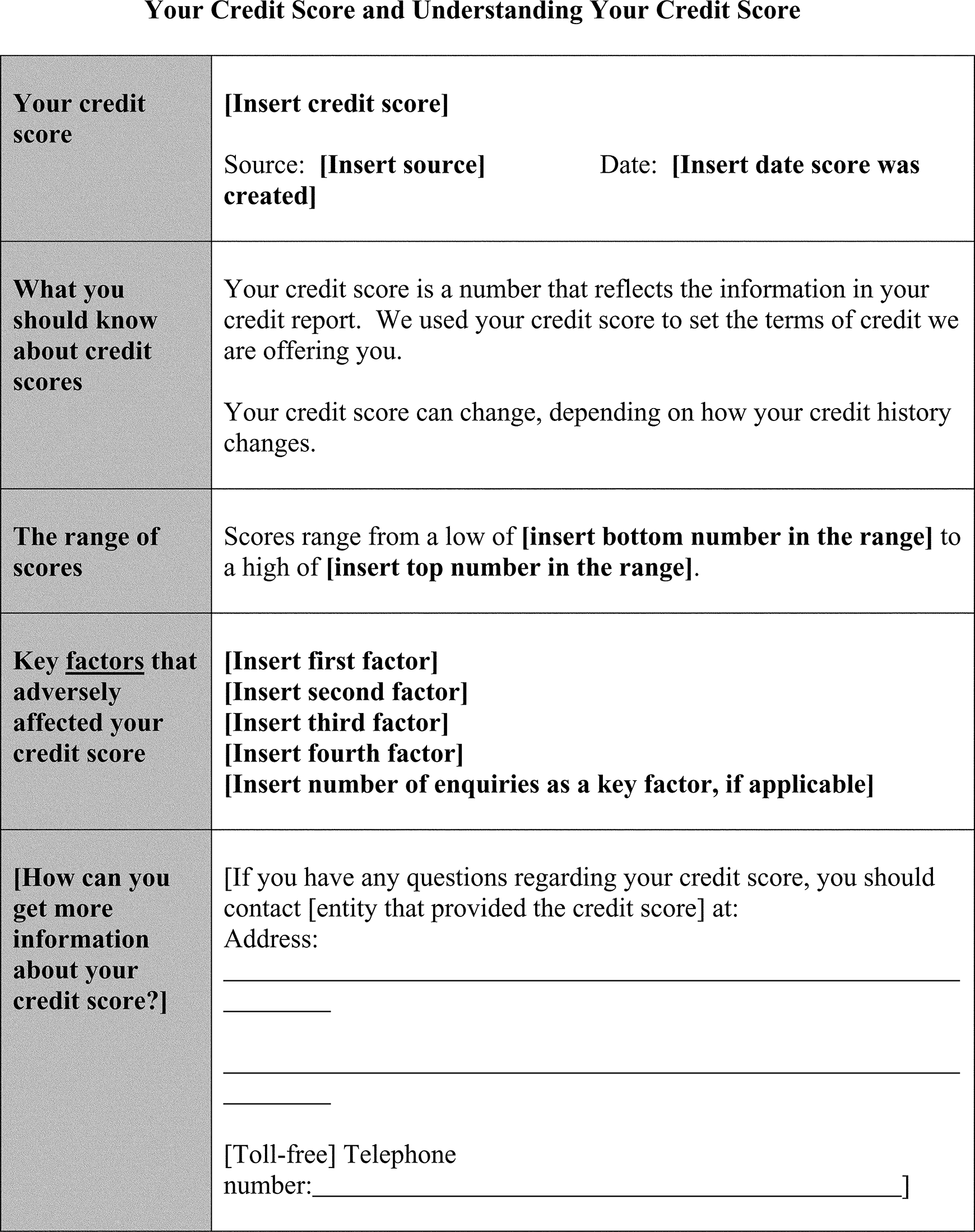

2. Model form H-1 is for use in complying with the general risk-based pricing notice requirements in Sec. 1022.72 if a credit score is not used in setting the material terms of credit. Model form H-2 is for risk-based pricing notices given in connection with account review if a credit score is not used in increasing the annual percentage rate. Model form H-3 is for use in connection with the credit score disclosure exception for loans secured by residential real property. Model form H-4 is for use in connection with the credit score disclosure exception for loans that are not secured by residential real property. Model form H-5 is for use in connection with the credit score disclosure exception when no credit score is available for a consumer. Model form H-6 is for use in complying with the general risk-based pricing notice requirements in Sec. 1022.72 if a credit score is used in setting the material terms of credit. Model form H-7 is for risk-based pricing notices given in connection with account review if a credit score is used in increasing the annual percentage rate. All forms contained in this appendix are models; their use is optional.

3. A person may change the forms by rearranging the format or by making technical modifications to the language of the forms, in each case without modifying the substance of the disclosures. Any such rearrangement or modification of the language of the model forms may not be so extensive as to materially affect the substance, clarity, comprehensibility, or meaningful sequence of the forms. Persons making revisions with that effect will lose the benefit of the safe harbor for appropriate use of appendix H model forms. A person is not required to conduct consumer testing when rearranging the format of the model forms.

a. Acceptable changes include, for example:

i. Corrections or updates to telephone numbers, mailing addresses, or Web site addresses that may change over time.

ii. The addition of graphics or icons, such as the person's corporate logo.

iii. Alteration of the shading or color contained in the model forms.

iv. Use of a different form of graphical presentation to depict the distribution of credit scores.

v. Substitution of the words “credit” and “creditor” or “finance” and “finance company” for the terms “loan” and “lender.”

vi. Including pre-printed lists of the sources of consumer reports or consumer reporting agencies in a “check-the-box” format.

vii. Including the name of the consumer, transaction identification numbers, a date, and other information that will assist in identifying the transaction to which the form pertains.

viii. Including the name of an agent, such as an auto dealer or other party, when providing the “Name of the Entity Providing the Notice.”

ix. Until January 1, 2013, substituting “For more information about credit reports and your rights under Federal law, visit the Federal Reserve Board's Web site at www.federalreserve.gov, or the Federal Trade Commission's Web site at www.ftc.gov.” for “For more information about credit reports and your rights under Federal law, visit the Consumer Financial Protection Bureau's Web site at www.consumerfinance.gov/learnmore.”

b. Unacceptable changes include, for example:

i. Providing model forms on register receipts or interspersed with other disclosures.

ii. Eliminating empty lines and extra spaces between sentences within the same section.

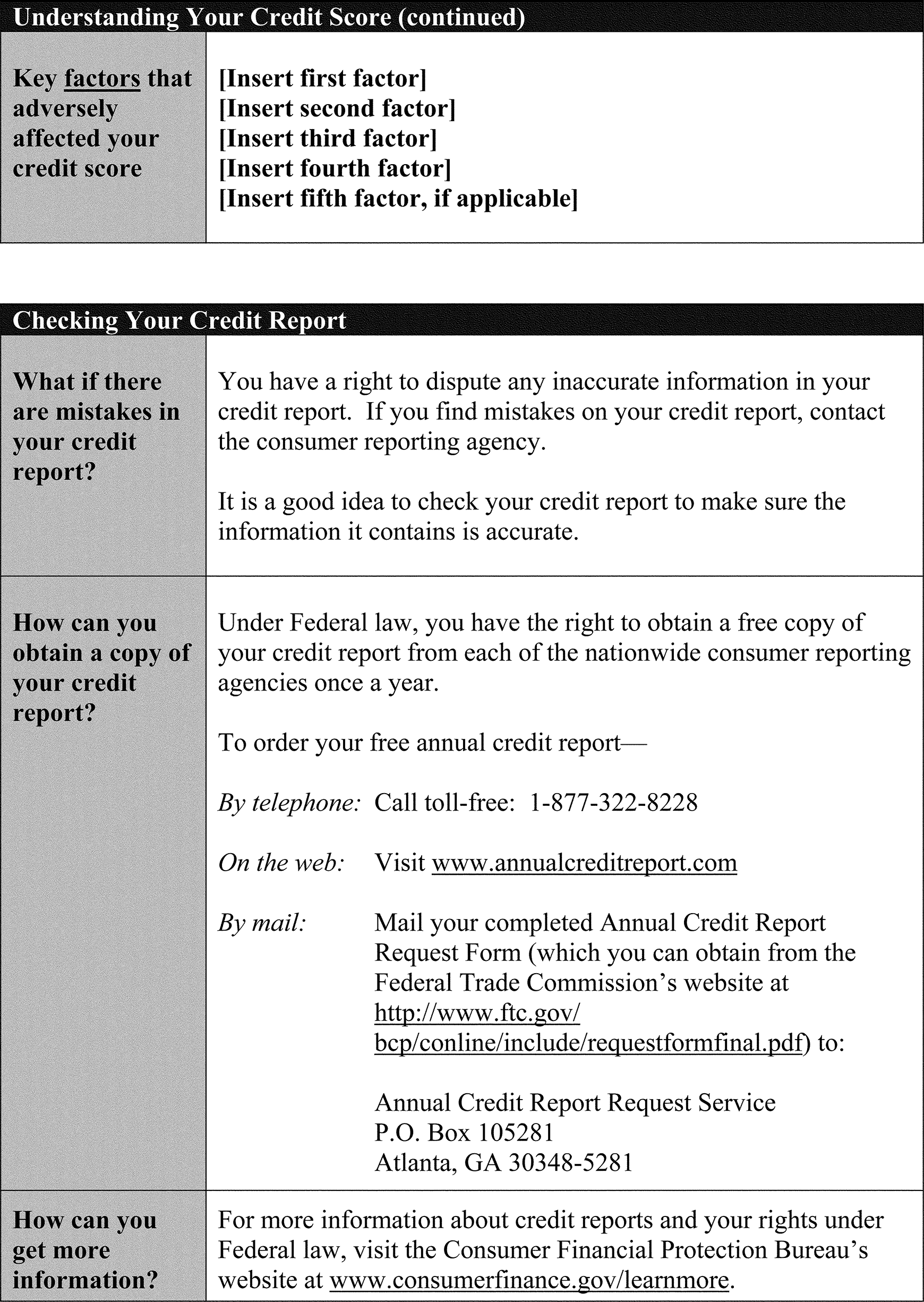

4. If a person uses an appropriate appendix H model form, or modifies a form in accordance with the above instructions, that person shall be deemed to be acting in compliance with the provisions of § 1022.73 or § 1022.74, as applicable, of this part. It is intended that appropriate use of Model Form H-3 also will comply with the disclosure that may be required under section 609(g) of the FCRA. Optional language in model forms H-6 and H-7 may be used to direct the consumer to the entity (which may be a consumer reporting agency or the creditor itself, for a proprietary score that meets the definition of a credit score) that provided the credit score for any questions about the credit score, along with the entity's contact information. Creditors may use or not use the additional language without losing the safe harbor, since the language is optional.

H-1 Model form for risk-based pricing notice.

H-2 Model form for account review risk-based pricing notice.

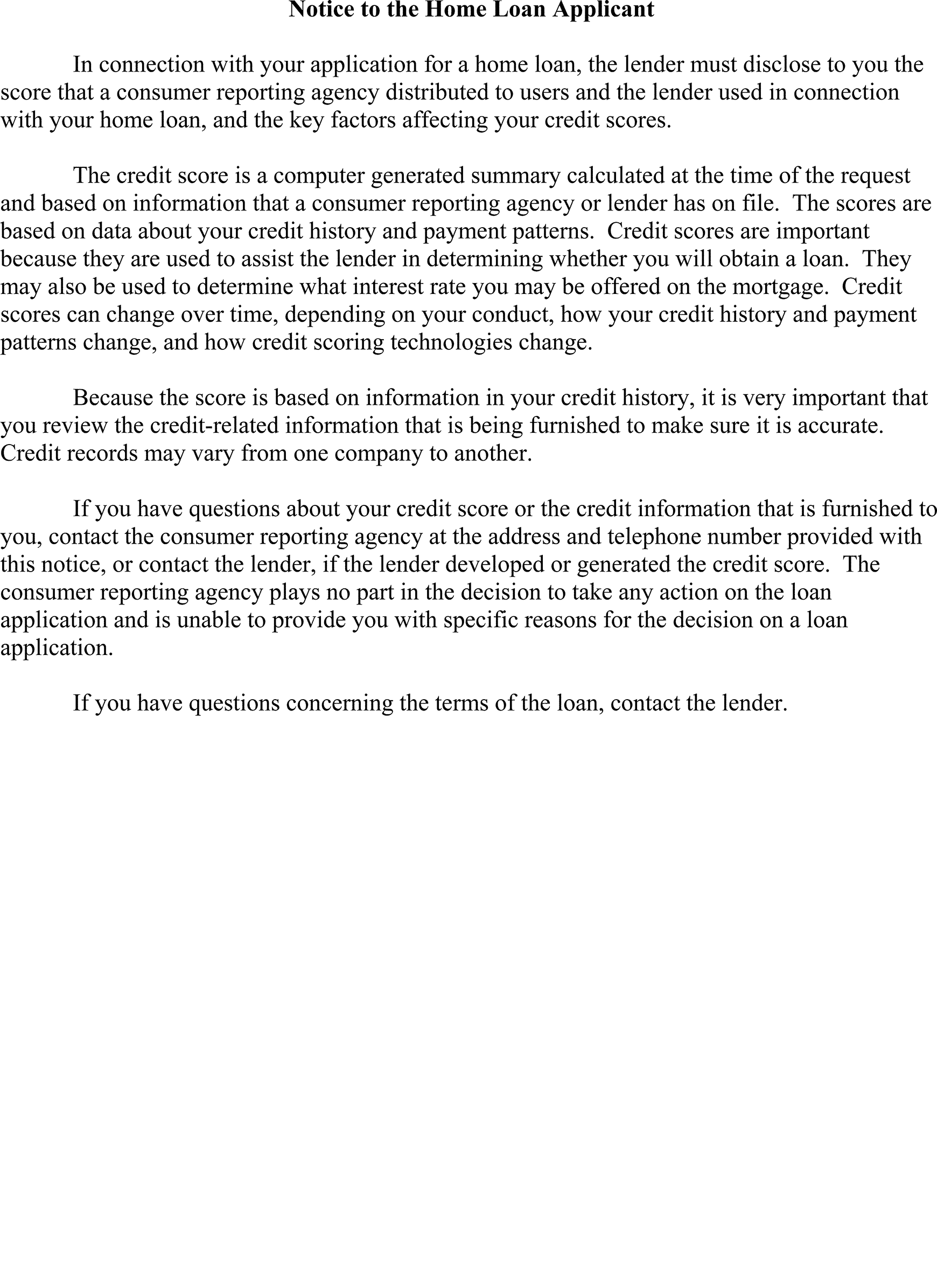

H-3 Model form for credit score disclosure exception for credit secured by one to four units of residential real property.

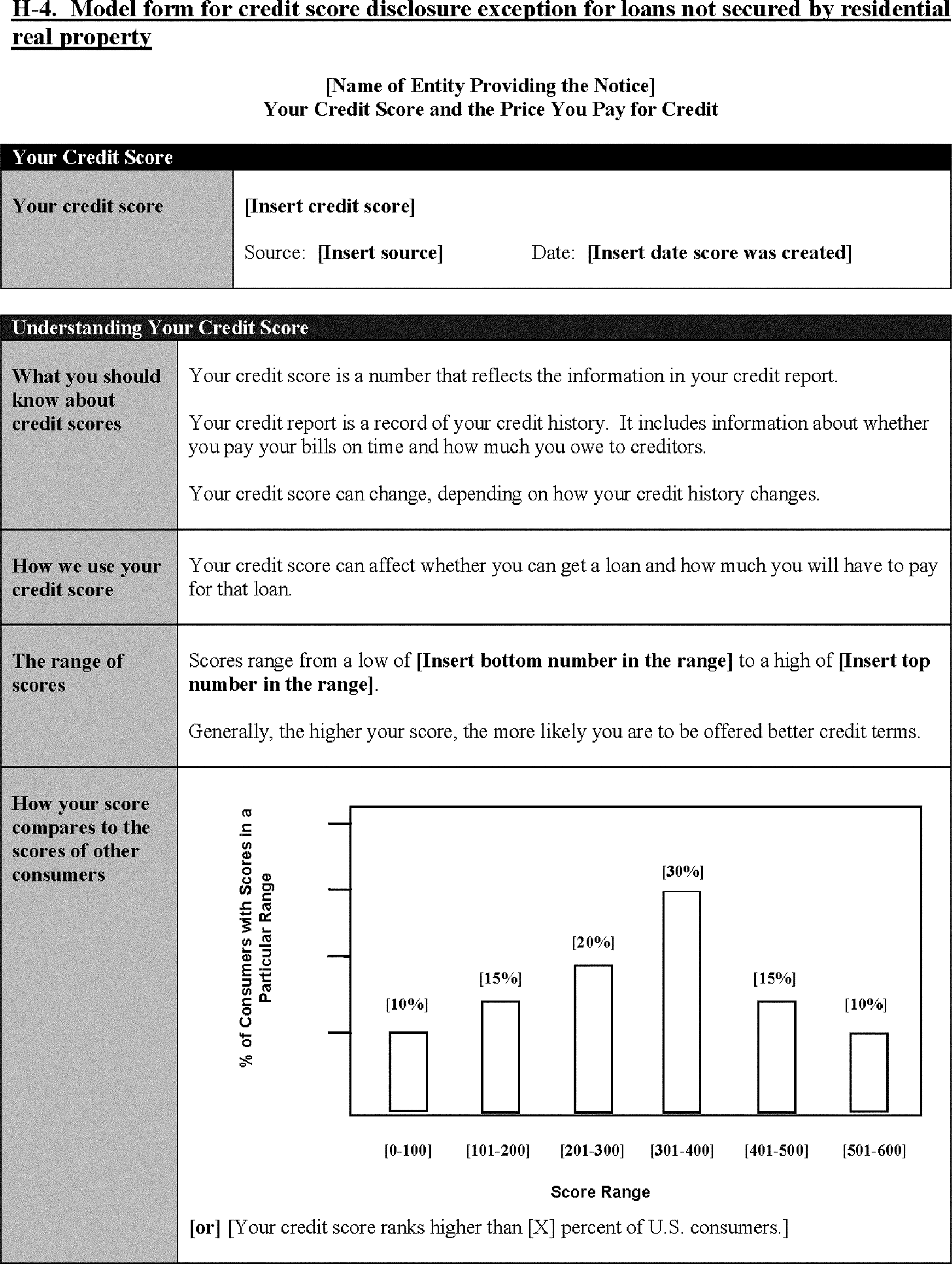

H-4 Model form for credit score disclosure exception for loans not secured by residential real property.

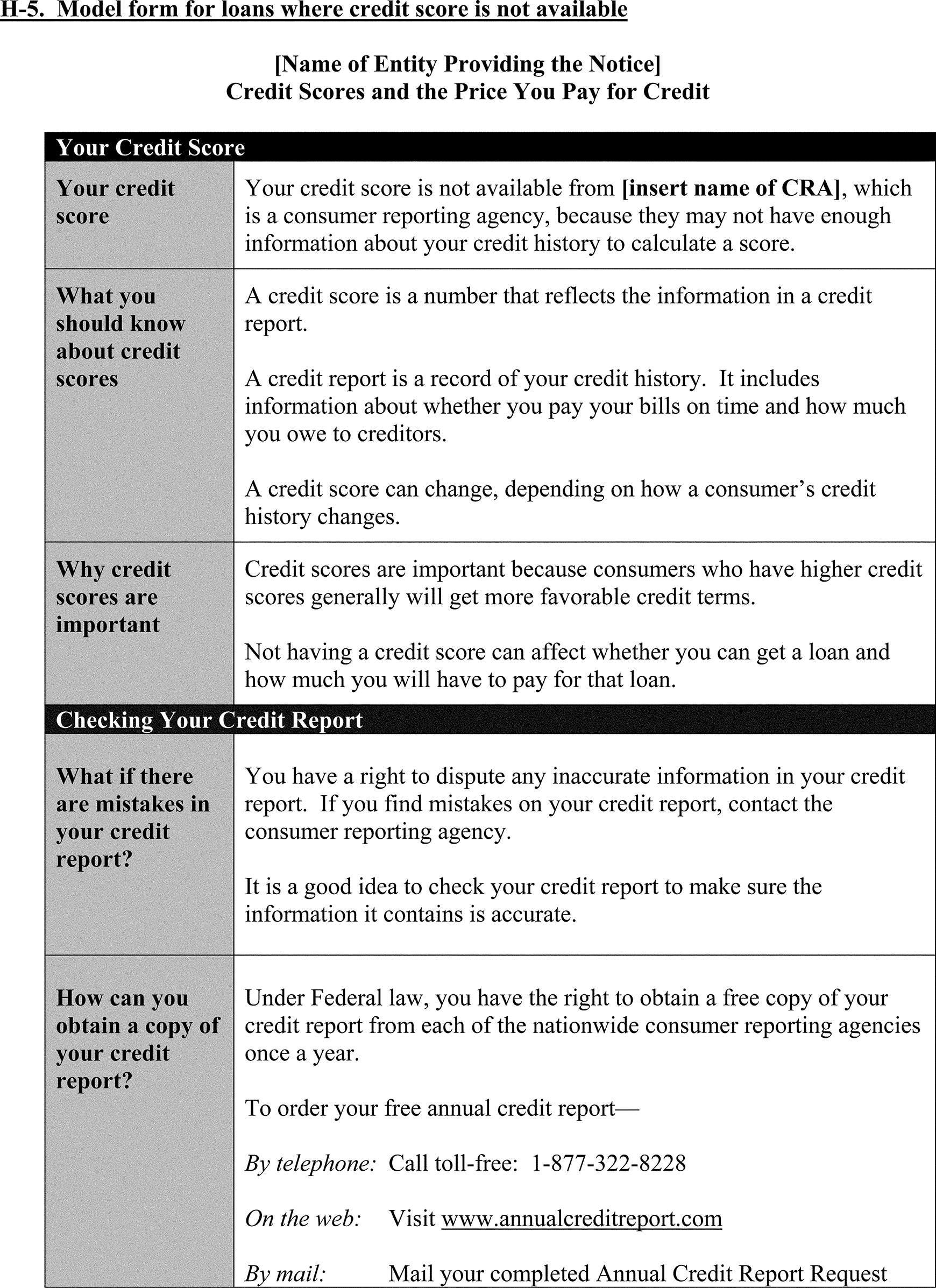

H-5 Model form for credit score disclosure exception for loans where credit score is not available.

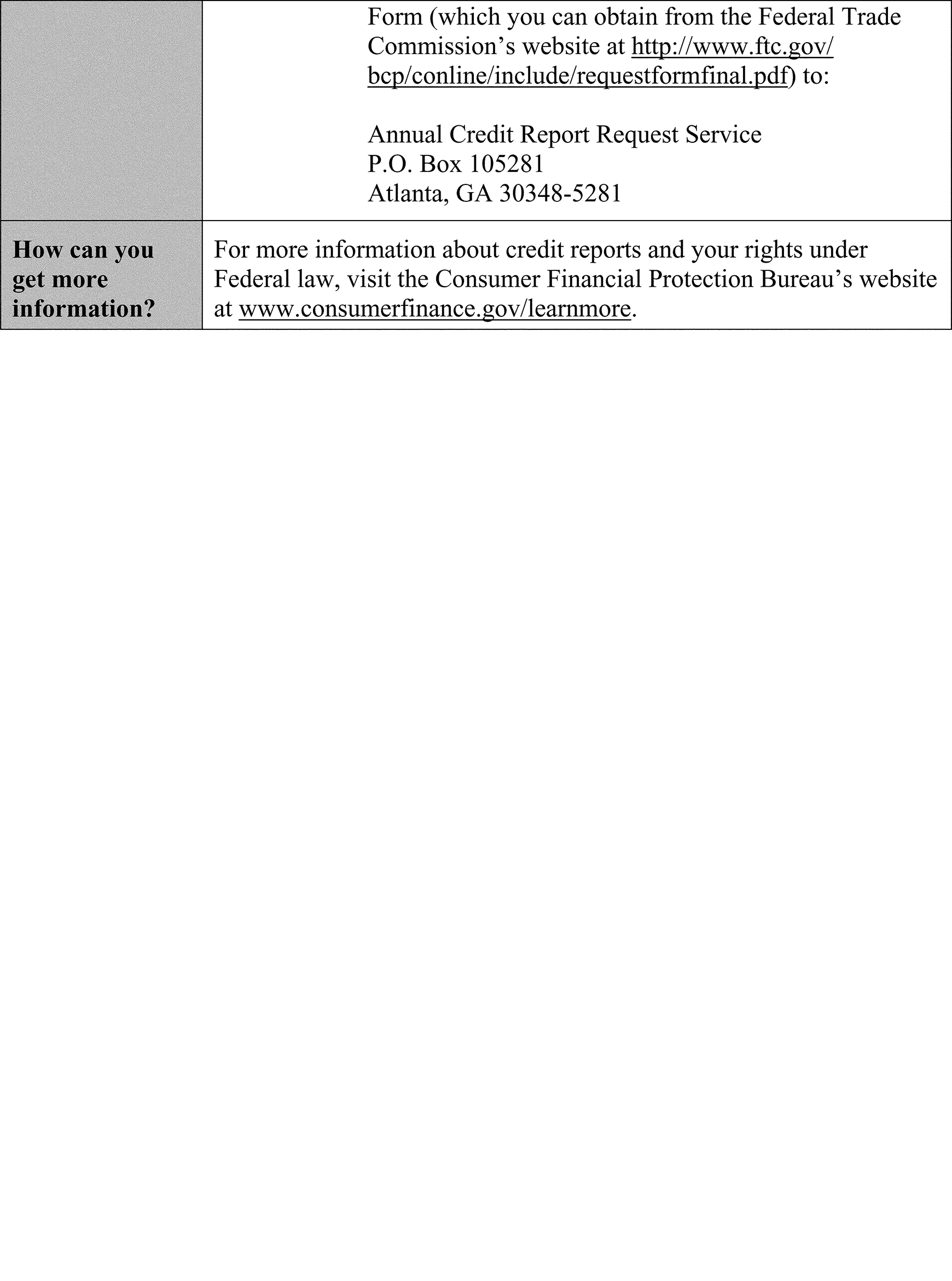

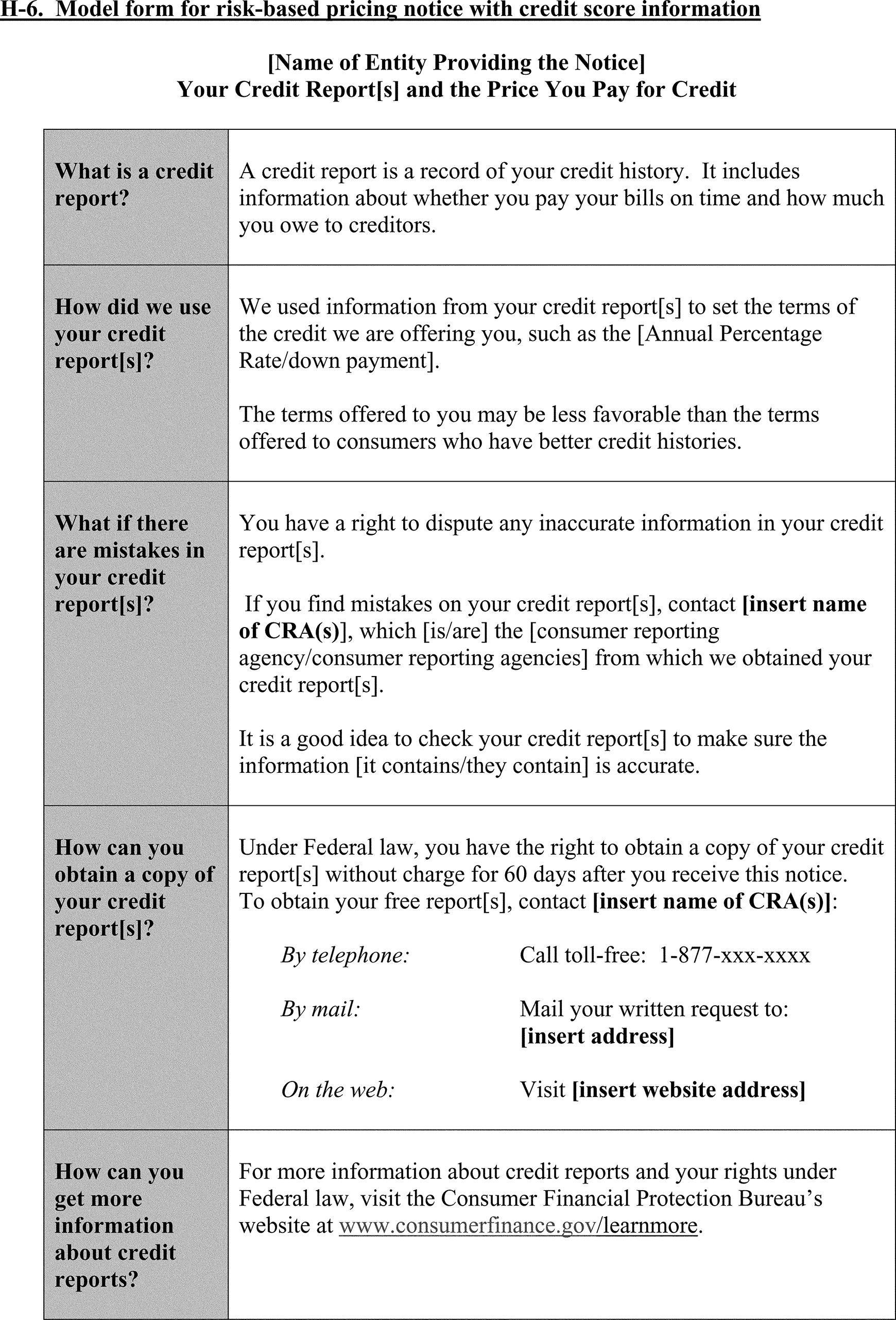

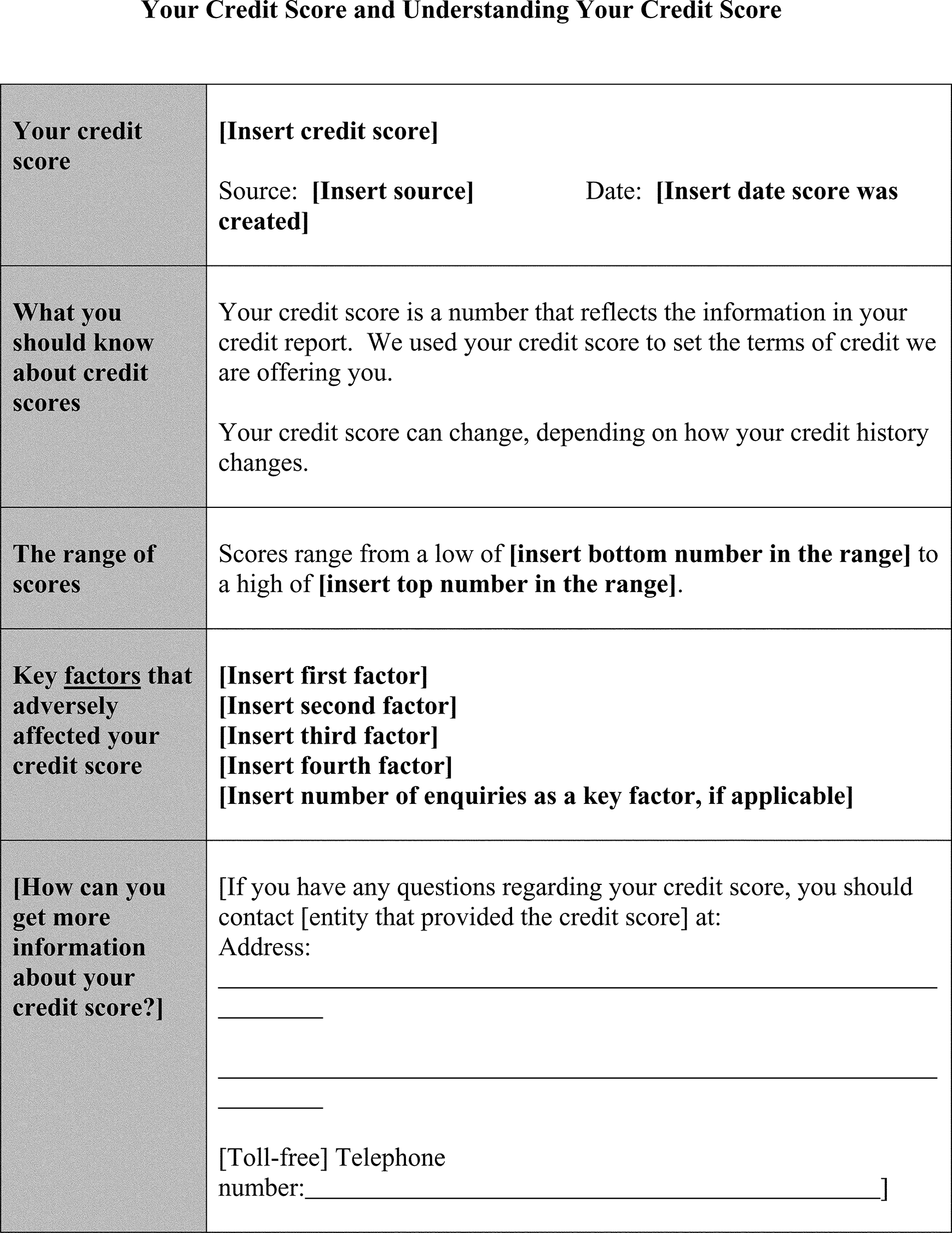

H-6 Model form for risk-based pricing notice with credit score information.

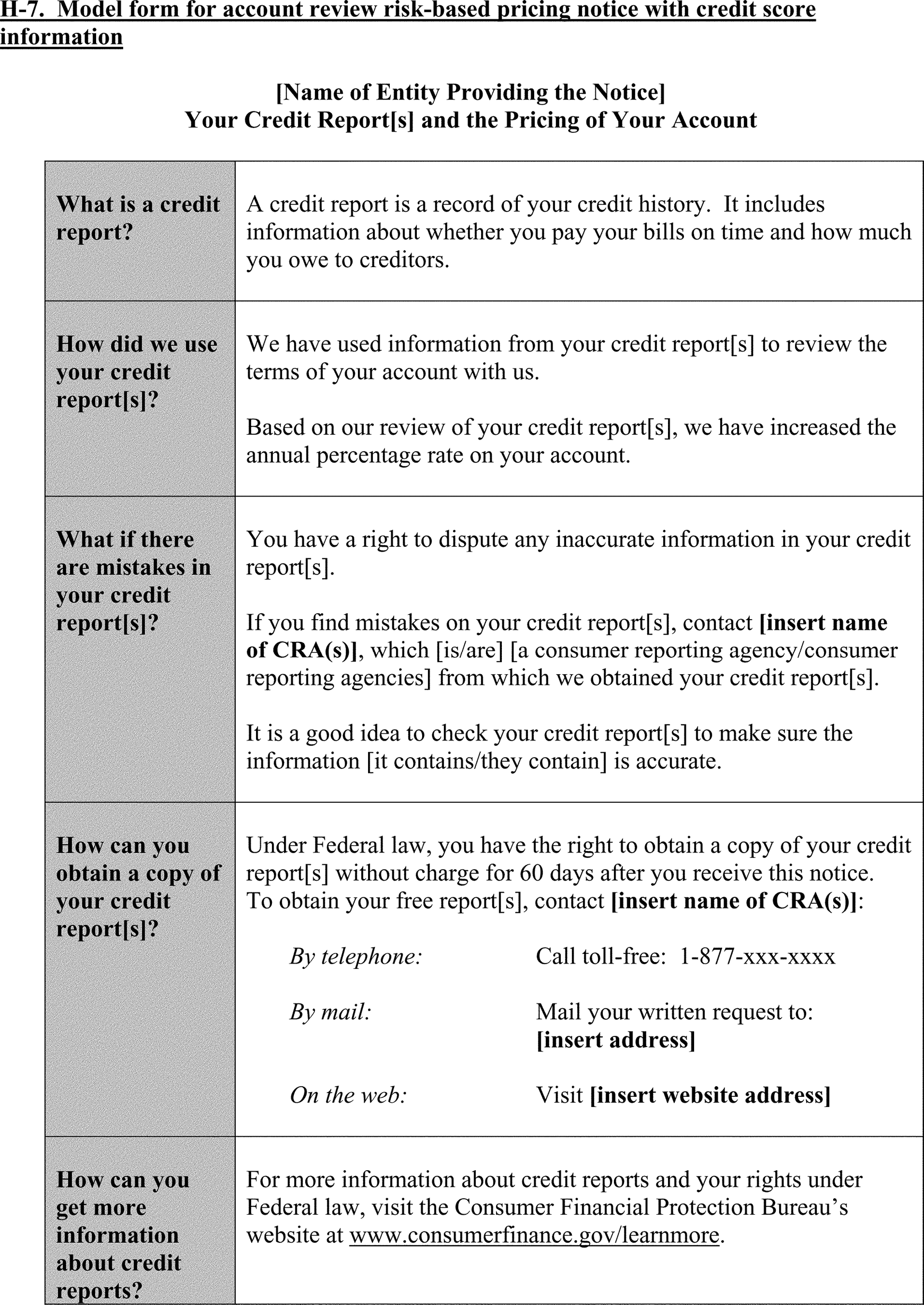

H-7 Model form for account review risk-based pricing notice with credit score information.